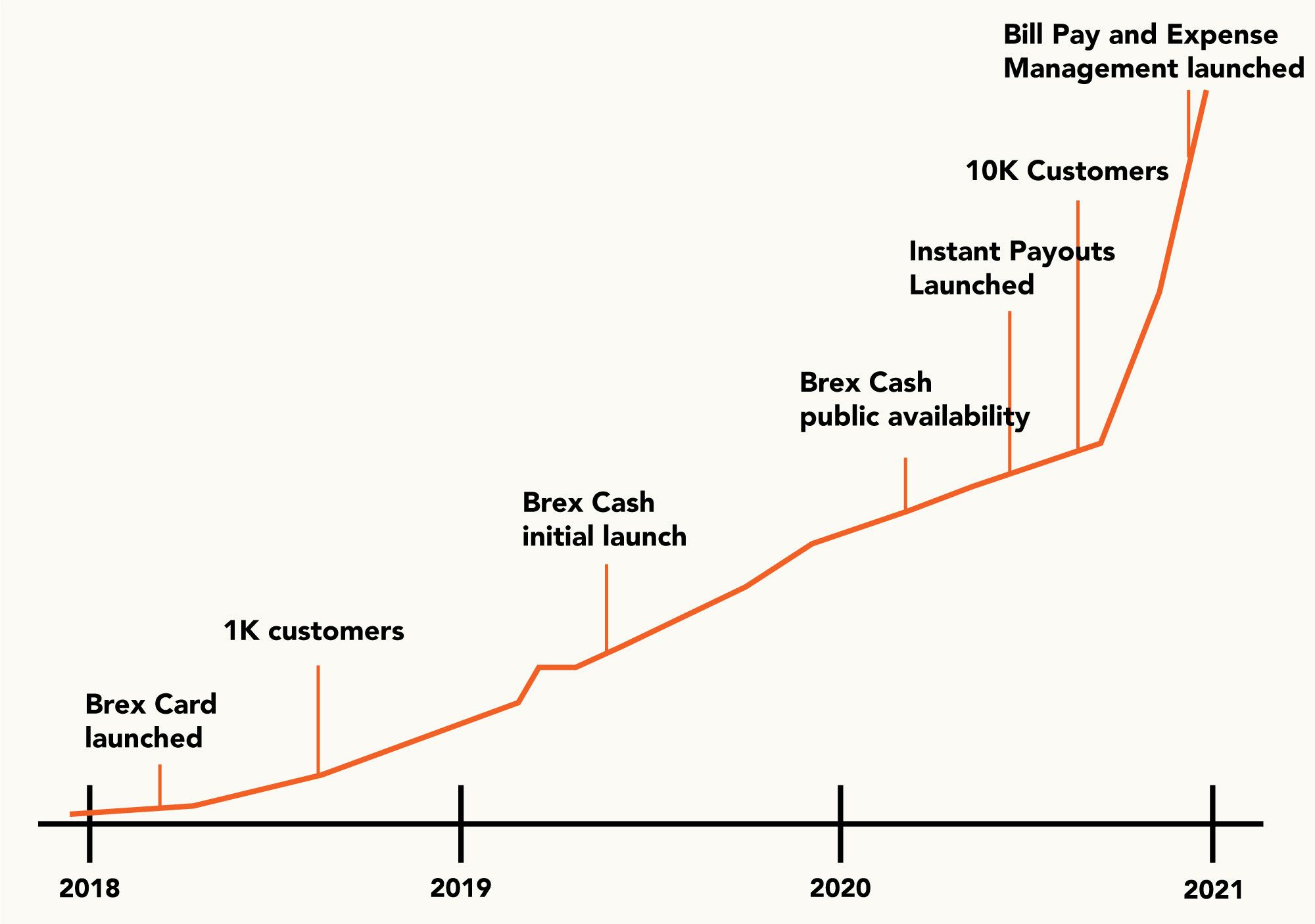

deep dives</a> on the problems and what they did to fix them.</p><p>As Monzo has scaled to become the leading neobank in the UK, it has continued to mindfully launch features with an emphasis on treating customers fairly and having a positive social impact. Our five favorite examples are outlined below:</p><p><strong><strong>(1) Gambling block:</strong></strong> One of the features that best highlights Monzo’s commitment to better money management is <a href=https://www.ycombinator.com/"https://monzo.com/i/gambling-block/">Gambling Block</a>, a feature where customers can disable transactions tagged as gambling. This feature might seem counterintuitive for banks traditionally incentivized to maximize monthly spend and revenue. But Monzo’s employees enthusiastically believed Gambling Block advanced the company’s customer-centric vision by encouraging better spending habits. The feature was actually devised by a small team of Monzonauts during “Monzo Time,” a monthly event during which employees can work on anything important to them. As of February 2021, Gambling Block was being used by 275,000 customers and was blocking nearly 600,000 transactions per month.</p><p><strong><strong>(2) Tone of voice guide:</strong></strong> In 2017, Monzo published a <a href=https://www.ycombinator.com/"https://monzo.com/tone-of-voice//">Tone of Voice</a> guide to maintain its clear, concise, positive voice as it scaled. This includes everything from Monzo’s terms and conditions, which have the required <a href=https://www.ycombinator.com/"https://monzo.com/blog/2018/07/02/the-monzo-mission/">reading age of 11</a>, to the way customer support agents communicate with customers.</p><p><strong><strong>(3) Proactive transparency:</strong></strong> Like all banks, Monzo has visibility into customer spending. Unlike all banks, Monzo uses this visibility to go above and beyond in proactively supporting users. In 2018, Monzo’s financial crime and security team noticed a concentrated number of fraudulent Ticketmaster transactions and immediately updated its systems to block suspicious transactions, alerted relevant parties, and <a href=https://www.ycombinator.com/"https://twitter.com/dan_graf/status/986979971905310720/">proactively replaced</a> customers’ cards. Two months after receiving information from Monzo, <a href=https://www.ycombinator.com/"https://monzo.com/blog/2018/06/28/ticketmaster-breach/">Ticketmaster announced the breach</a> that compromised card details.</p><p><strong><strong>(4) Fair-use fees and customer-friendly lending:</strong></strong> In 2020, Monzo introduced <a href=https://www.ycombinator.com/"https://monzo.com/blog/withdrawal-and-card-delivery-fees/">fair-use fees</a> for customers who used certain features above normal levels and created higher levels of free allowances for customers who used Monzo as their main account. The new fees impacted fewer than 30% of Monzo customers and were well-received by the community. Another example of Monzo’s customer-centric approach is <a href=https://www.ycombinator.com/"https://monzo.com/flex//">Monzo Flex</a>, which is a better way to pay later. Instead of just launching another BNPL product, Monzo asked customers what they liked and disliked about existing lending products. Customers told them they didn’t want to have to reapply every purchase, they wanted flexible payment terms, and they wanted ubiquitous acceptance. Monzo Flex solves these problems by checking for affordability and letting users spread the cost across any purchase with flexible payment terms.</p><p><strong><strong>(5) Internal inclusion goals:</strong></strong> Monzo’s company operating system was also designed with transparency, fairness, and authenticity. The company publishes <a href=https://www.ycombinator.com/"https://monzo.com/blog/our-2020-diversity-and-inclusion-report/">an annual report</a> of its progress on diversity and is on track to reach a <a href=https://www.ycombinator.com/"https://monzo.com/blog/gender-pay-gap-update-april-2020-and-april-2021/">0% gender pay gap</a>. Women make up 40% of their executive team and board. This focus on building an inclusive company operating system is one of the many reasons why Monzo is consistently rated the <a href=https://www.ycombinator.com/"https://www.linkedin.com/pulse/linkedin-top-startups-2021-15-uk-companies-rise-linkedin-news-uk//">number one UK startup</a> on LinkedIn.</p><p>In 2019, Monzo was recognized by <a href=https://www.ycombinator.com/"https://monzo.com/blog/monzo-is-the-uks-most-recommended-brand/">YouGov as not just the most-recommended bank but <u>consumer brand</u>, and in 2020 it was rated the number-one bank for service quality per the <a href=https://www.ycombinator.com/"https://monzo.com/blog/2020/08/17/were-the-best-bank-for-overall-service-quality-and-online-and-mobile-banking/">Competition and Markets Authority</a>. Monzo’s efforts to build a customer centric brand and their focus on building a best-in-class consumer product helped the company scale from 500 to 500,000 users less than 24 months after initial Alpha launch and less than 6 months after launching full bank accounts.</p><h2 id=\"scaling-monzo-growing-to-5m-users-and-100k-businesses-in-5-years\"><strong>Scaling Monzo: Growing to 5M+ users and 100K businesses in 5 years</strong></h2><p>Monzo’s second chapter has been even more impressive. Since launching in the UK five years ago, Monzo has scaled to 5.3 million users, or more than 10% of the adult population. In an incredibly short amount of time, Monzo has managed to turn a good product into a highly competitive platform with a significant market share. And they did it by spending only £20M on marketing in one year, or <£20 per customer. In the years since, they’ve spent £0 on marketing.</p><p><strong><strong>Scaling the customer base efficiently and effectively</strong></strong><br>Monzo used its early enthusiastic community to drive new customer growth. In designing its cards, Monzo chose an eye-catching hot coral color. The card became a conversation piece, as curious bystanders asked Monzo customers about it, which would naturally result in new signups. Monzo then built social features to supercharge word-of-mouth growth. It launched <a href=https://www.ycombinator.com/"https://monzo.com/blog/2016/10/17/wonderful-surprises/">Golden Tickets</a> that customers could give to their friends to skip the waitlist, peer-to-peer payments, and contact list sharing between friends. These social features accelerated user growth to 5% week-over-week and helped Monzo scale to over one million users with effectively zero marketing spend in a sector where customers typically cost <a href=https://www.ycombinator.com/"https://www.which.co.uk/news/2021/08/nationwide-launches-125-switching-bonus-is-it-worth-it//">£100–150 to acquire. Today, the average user has 30 friends on Monzo and 83% of active customers enable P2P payments within their first year. Like “Venmo me” in the US, “Monzo me” has become a fixture in the UK vernacular.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-04-p2p.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><p>Monzo also expanded its product from a spending account to full-fledged bank account and financial control center. In its first few years, Monzo added basic banking features such as overdrafts, cash deposits, and direct debits to reach feature parity with traditional banking. In the past 18 months, Monzo revamped personal loans and launched premium subscription accounts with software features and perks such as third-party spend and savings tracking, virtual cards, custom categories, credit tracking, exclusive merchant discounts, and insurance. Today, Monzo isn’t just a complete bank replacement; it’s the best consumer banking experience in the world.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-05-consumer-banking.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><p>Monzo has successfully scaled its customer support and banking infrastructure alongside its user base. There is an entire product team dedicated to building software for customer support agents to surface customer information in seconds and maintain a consistent customer voice across every interaction. This is an enduring advantage over peers that rely on third-party software or automated support systems.</p><p>Monzo has also scaled its internal banking infrastructure. When it first launched, Monzo partnered with third-party payment processors to get to market quickly. Over time, Monzo migrated to internal systems and now has the lowest downtime in the entire banking industry (incumbents and startups). With these backend improvements, Monzo has been able to grow from a tiny startup to a major banking platform while maintaining a 70 NPS. In 2021, over 40% of active customers were using Monzo as their main account, up more than 10 percentage points from 2020.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-06-account-usage.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><p><strong><strong>A natural transition to business banking</strong></strong><br>As Monzo’s consumer brand scaled, the team saw an opportunity to launch a banking product for small and medium businesses (SMBs) in the UK. The average business has 6x more deposits than the average consumer customer and Monzo already had more than 250,000 customers that owned a small business. Legacy banks were not meeting SMB needs, with the average business using 10 to 15 different financial products because SMB accounts were designed solely as transaction accounts. To solve this, Monzo launched business banking as a spending account with added software features such as invoicing, tax budgets, multi-user access, and accounting integrations. Since their SMB launch in April 2020, Monzo has organically scaled to over 100,000 businesses, outpacing every competitor. It took their closest competitor two years and significant marketing spend to reach the same scale.</p><p>Looking ahead, the company has an opportunity to serve larger businesses as well, by building financial operations tooling such as payables/receivables software and international payment capabilities. At scale, Monzo will be also uniquely positioned to enable seamless interactions between business customers and personal customers, similar to how Square does in the US.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-07-business-banking.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><h2 id=\"monzo%E2%80%99s-opportunity-a-leading-consumer-and-business-finance-platform\"><strong>Monzo’s opportunity: A leading consumer and business finance platform</strong></h2><p>The success of Monzo’s first five years will naturally lead to continued expansion within and outside of the UK. We think these are the most exciting opportunities for Monzo to disrupt the global banking landscape:</p><p><strong><strong>(1) Using great software to drive deep value for customers:</strong></strong> Monzo is able to maintain customer-friendly fee structures and policies simply by cutting significant infrastructure operating costs. Their subscription banking product, which offers virtual cards, third-party account connections, and advanced budgeting features in exchange for a flat fee is fundamentally disruptive to incumbents. Today, Monzo’s long-term retention of premium customers outperforms incumbent financial services and is more inline with best-in-class consumer subscription companies like Calm, Netflix, and Spotify. Incumbents do not have the engineering talent or infrastructure to compete.</p><p><strong><strong>(2) Leveraging its two-sided network to build unique customer experiences:</strong></strong> Because of its single-country focus, Monzo has been able to achieve deep reach among both consumer and SMB banking customers in the UK. The company now serves 10% of UK consumers, has 50%+ of UK neobank market share, and has 100,000 SMB customers. The company is in a unique position to build a consumer-to-business payment network in the UK, and has started to lay the foundation with products to <a href=https://www.ycombinator.com/"https://monzo.com/blog/2021/10/12/getting-paid-with-monzo-business/">help businesses get paid</a> and <a href=https://www.ycombinator.com/"https://monzo.com/flex//">Monzo Flex</a>.</p><p>With Monzo’s business payments product, SMBs can collect payments via credit card and bank transfers, historically a huge pain point. Instead of sending invoices via email, businesses can send a Monzo payment link to customers. Early data shows high repeat usage, with the experience being meaningfully better when both the SMB and customer are Monzo users. As its two-sided network scales, more money will stay entirely within the Monzo ecosystem, resulting in better economics and experiences for both the company and its customers.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-08-business-payment-tools.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><p><a href=https://www.ycombinator.com/"https://monzo.com/flex//">Monzo Flex</a> is another product that benefits both consumers and businesses. Flex lets users finance purchases over £30 across multiple installments. Monzo’s natural visibility into users’ spending and financial health enables it to create a product that is better for consumers than traditional BNPL options. First, Monzo finances any transaction (offline or online) regardless of merchant partnership. Second, Monzo leverages its banking relationship to run affordability checks on users. This means Monzo will not approve Flex purchases for customers likely to end up in an endless cycle of debt. Traditional BNPL players can’t do this because it threatens their business model of prioritizing spend and merchant conversion. Over time, Monzo can even leverage its scale in the UK to sign partnerships with merchants to reduce costs for consumers. Flex could also disrupt the credit card market, as users use their virtual Flex cards instead of credit cards to finance payments. While early, the company has seen incredible demand for Flex only a few months after launch.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-09-flex.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><p><strong><strong>(3) Launching new financial tools:</strong></strong> The UK banking market remains fairly disaggregated. A customer might use Monzo for banking, eToro for crypto, Freetrade for equities, and Atom for a mortgage. Monzo will continue to expand its offerings through both its own products and third-party partnerships (where Monzo acts as the front end or distribution engine). As one example, Monzo launched a savings marketplace for customers to earn additional returns two years ago. This product scaled to ~£1.5B in deposits and ~15% penetration of its customer base during a period of near-0% interest rates, creating value for both customers (by offering them higher returns) and deposit partners (who would otherwise have to pay large acquisition costs). Over time, Monzo will have increased opportunities to create new experiences for users in investing, crypto (e.g., staking, buying/selling), savings, and lending.</p><p><strong><strong>(4) Expanding internationally:</strong></strong> The company has spent the last 12 months laying the foundation for its US launch. Rather than copy-pasting its home features to new geographies, Monzo is taking the same user-first design and community approach that won it the dominant position in the UK market. Monzo is running US-based community events, publishing a <a href=https://www.ycombinator.com/"https://app.productstash.io/monzo-usa-public-roadmap/">public product roadmap</a>, and consistently adding new features. Monzo has already scaled the US product to 6,000 beta users and has 38,000 users on its waitlist. But unlike when it launched in the UK, Monzo now has five years of history and product work to leverage. This has enabled Monzo to launch features much faster in the US. Because of its strong foundation and country-specific product approach, Monzo is positioned to become a global financial platform and a major banking institution in every market it enters.</p><h2 id=\"conclusion-spend-save-and-manage-your-money-in-one-place\"><strong>Conclusion: Spend, save, and manage your money in one place</strong></h2><p>Five years in, Monzo is just starting its second act. Monzo’s first act was to build the UK’s best consumer and SMB banking product. Their second act will be to make money work for truly everyone by scaling to a global audience. Over the next decade, the global market share of financial services will increasingly shift towards financial technology companies. We are already seeing signs of this shift within YC. Companies like Brex, Groww, Jeeves, Parker, and Point are capturing share from incumbents in their respective markets. Monzo will be one of the main beneficiaries of this shift, as it continues to compound its lead in the UK and drive growth in new markets.</p><p><em><em>Thank you to Max Winston, the entire Monzo team, Mia Mabanta, and Chloe Gordon for reading multiple drafts of this essay, and to Zain Ali for designing the graphics.</em></em></p><hr><p><sup><strong>1</strong></sup> Financial Conduct Authority – Strategic Review of Retail Banking Business Models <a href=https://www.ycombinator.com/"https://blog.ycombinator.com/monzo-makes-money-work-for-everyone/#footnoteid1\">↩</a><br><sup><strong>2</strong></sup> YC UK Survey on Consumer Banking – 2018 <a href=https://www.ycombinator.com/"https://blog.ycombinator.com/monzo-makes-money-work-for-everyone/#footnoteid2\">↩</a><br><sup><strong>3</strong></sup> Data from Monzo <a href=https://www.ycombinator.com/"https://blog.ycombinator.com/monzo-makes-money-work-for-everyone/#footnoteid3\">↩</a><br><sup><strong>4</strong></sup> Public Filings and FCA’s Retail Banking Market Investigation <a href=https://www.ycombinator.com/"https://blog.ycombinator.com/monzo-makes-money-work-for-everyone/#footnoteid4\">↩</a></p>","comment_id":"61ba442d495e820001cd7ac6","feature_image":"/blog/content/images/2021/12/monzo-01.jpg","featured":false,"visibility":"public","email_recipient_filter":"none","created_at":"2021-12-15T11:38:21.000-08:00","updated_at":"2022-01-29T19:00:42.000-08:00","published_at":"2021-12-08T11:39:00.000-08:00","custom_excerpt":"Scaling a startup is hard. Scaling a startup bank is even harder. Scaling a consumer-focused financial platform—that is also now the primary bank account for millions of UK consumers—in the midst of a once in a century pandemic is close to impossible.","codeinjection_head":null,"codeinjection_foot":null,"custom_template":null,"canonical_url":null,"authors":[{"id":"61fe29e3c7139e0001a710b2","name":"Nic Dardenne","slug":"nic-dardenne","profile_image":"/blog/content/images/2022/02/Nic.jpg","cover_image":null,"bio":"Nic is a principal at YC Continuity. Nic has helped support the teams at Brex, Convoy, Faire, Groww, Monzo, Rappi, Segment, Snapdocs, and Vouch. Before YC, Nic worked as an analyst at Morgan Stanley.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/nic-dardenne/"},{"id":"61fe29e3c7139e0001a7107b","name":"Anu Hariharan","slug":"anu-hariharan","profile_image":"/blog/content/images/2022/02/Anu.png","cover_image":null,"bio":"Anu is a Managing Director & Partner at YC Continuity. Previously, Anu was a Partner at a16z, where she worked actively with the management teams of companies including Airbnb, Instacart, and Medium.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/anu-hariharan/"}],"tags":[{"id":"61fe29efc7139e0001a7116d","name":"Essay","slug":"essay","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/essay/"},{"id":"61fe29efc7139e0001a71170","name":"Startups","slug":"startups","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/startups/"},{"id":"61fe29efc7139e0001a71182","name":"#ycc","slug":"hash-ycc","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"61fe29efc7139e0001a71181","name":"YC Continuity","slug":"yc-continuity","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/yc-continuity/"},{"id":"61fe29efc7139e0001a711b6","name":"#4787","slug":"hash-4787","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"}],"primary_author":{"id":"61fe29e3c7139e0001a710b2","name":"Nic Dardenne","slug":"nic-dardenne","profile_image":"https://ghost.prod.ycinside.com/content/images/2022/02/Nic.jpg","cover_image":null,"bio":"Nic is a principal at YC Continuity. Nic has helped support the teams at Brex, Convoy, Faire, Groww, Monzo, Rappi, Segment, Snapdocs, and Vouch. Before YC, Nic worked as an analyst at Morgan Stanley.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/nic-dardenne/"},"primary_tag":{"id":"61fe29efc7139e0001a7116d","name":"Essay","slug":"essay","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/essay/"},"url":"https://ghost.prod.ycinside.com/monzo-makes-money-work-for-everyone/","excerpt":"Scaling a startup is hard. Scaling a startup bank is even harder. Scaling a consumer-focused financial platform—that is also now the primary bank account for millions of UK consumers—in the midst of a once in a century pandemic is close to impossible.","reading_time":15,"access":true,"og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"email_subject":null,"frontmatter":null,"feature_image_alt":null,"feature_image_caption":null},{"id":"61fe29f1c7139e0001a71bf6","uuid":"a8119b6d-b3a3-482e-9263-f7b8c0865cea","title":"Gusto: The People Platform for SMBs","slug":"gusto-the-people-platform-for-smbs","html":"<!--kg-card-begin: html--><p>Historically, there has been an undeniable gap in business services in the US. There are nearly six million small and medium businesses (SMBs) in the country, employing 43 million people.<sup id=\"footnoteid1\"><a href=https://www.ycombinator.com/"#footnote1\">1</a></sup> But unlike their larger counterparts, SMBs have been ignored by service providers, who have deemed the cost of reaching and serving them too high to warrant the effort. As a result, SMBs have been forced to cobble together off-the-shelf products, spreadsheets, and manual work to run their operations.</p>\n<p>This gap is most visible in the payroll and benefits sectors. Even though companies like ADP and Paychex have existed for more than 50 years, about 30% of SMBs still manage payroll without the help of a third-party service.<sup id=\"footnoteid2\"><a href=https://www.ycombinator.com/"#footnote2\">2</a></sup></p>\n<p>There are three reasons why existing providers haven’t cracked small business payroll and benefits. First, SMBs are fragmented and hard to reach. Relative to the value they bring in, the cost of reaching and serving them has traditionally been too high to warrant the effort unless you can sell multiple products to them. Second, there is significant signup friction for benefits and payroll products. Lastly, benefits products can be costly for SMBs to offer to employees, which results in many just forgoing benefits altogether. The lack of access to simple payroll and benefits tools has had a significant impact on the operational efficiency of SMBs and the well-being of their employees. But where there is a gap, there is an opportunity.</p>\n<p>Gusto launched in 2012 to tackle this opportunity, and more. Josh Reeves, Tomer London, and Eddie Kim saw an opportunity to build a people-centered software platform for SMBs that would do three things: (1) bring peace of mind to the employer and employee around complex actions like payroll, benefits, setting up software, and more; (2) help build better places to work by focusing more on the employer-employee partnership; and (3) create personal prosperity for employees by helping supercharge the paycheck and providing access to better benefits. Gusto initially focused on building payroll because it was the most acute pain point, and it was a natural system of record for employee data and transactions. Payroll was the foundation for Gusto to achieve its vision of being a comprehensive “people platform.” Far beyond just paying employees and maintaining compliance, <strong>Gusto’s goal is to help employers build great places to work and run successful teams.</strong> And for employees, <strong>Gusto’s goal is to help put the individual in the driver’s seat of their financial health and their career.</strong> The name “Gusto” embodies the company’s mission to create a world where work empowers a better life—where work can be done “with Gusto.”</p>\n<p>The emergence of SaaS business models has further set the stage for companies like Gusto to transform SMB operations. With cloud-based software and automation, customers are cheaper to serve and simpler to onboard. In the long run, software platforms have the potential to be much larger than traditional incumbents. For customers, this will likely mean a significant bend in the cost curve for products and services. For SMBs specifically, this will lead to a meaningful boost financially and emotionally, and perhaps even higher degrees of company output. In this post, we will walk through Gusto’s journey from digital payroll provider to integrated people platform.</p>\n<h1>Act 1: Payroll: The Perfect Starting Point</h1>\n<p>When Gusto founders Josh, Tomer, and Eddie came together in 2011, they saw an unmet need in small business payroll. Despite the major players in the payroll space, 46% of SMBs in the US were spending more than three hours per month managing payroll logistics.<sup id=\"footnoteid3\"><a href=https://www.ycombinator.com/"#footnote3\">3</a></sup> On top of that, 40% were paying a penalty each year for incorrect payroll filings.<sup id=\"footnoteid4\"><a href=https://www.ycombinator.com/"#footnote4\">4</a></sup></p>\n<p>This was both an emotional and logistical pain point for SMB owners, with many becoming visibly upset as they talked to Josh, Tomer, and Eddie about it. Upon digging deeper, the founders realized that incumbent providers were overly complex, and more manual than necessary. For example, to become a customer of ADP or Paychex, SMBs had to go through a lengthy process of filling out paper forms and talking with sales reps. Once using the product, they had to rely on the provider’s human specialists to input information and manage the payroll process rather than doing it independently. For SMBs that had neither the hours nor resources to initiate these processes, this approach was untenable. In addition, the employee experience was an afterthought. Incumbent providers treated payroll as a transactional activity, often forcing people to log in using ID numbers and providing limited functionality once they did log in. This made for an impersonal experience for employers and employees alike, and created even more manual work and overhead for employers.</p>\n<p>Gusto saw an opportunity to upend the way payroll was done. First, by making payroll about people, not simply a transaction. And second, by bringing the strengths of modern software to this problem, using cloud, paperless, and mobile, to create a dramatically easier-to-use product. If the enrollment process were digitized and companies could access all aspects of payroll on their own time, barriers to getting set up and using the product would be removed. So Gusto began building a cloud-based engine that would allow SMBs to manage payroll with the click of a few buttons, and also make the employee an equally important user of the product instead of an afterthought.</p>\n<p>Building payroll architecture is complicated. It involves managing multiple systems (taxes, withholdings, filings, payments) in a reliable and compliant way. To run payroll correctly, a business must identify which taxes are applicable to which employee (there are thousands of options, usually determined by where an employee lives and works). The business must calculate and withhold the right tax amount, at the local, state, and federal levels. Then the business must determine how the taxes get paid, which is an equally complicated process. Some states want checks, others ACH debit/credit, and states and counties often require different payment timing. And then there are filings. Every destination for tax requires a separate filing—some printed, some faxed, some electronic. There are thousands of these filings, and the forms are each very different. Finally, the business needs to send the payment to the employee via ACH typically 1–2 days after running payroll, or write them a check by hand.</p>\n<p><img loading=\"lazy\" src=https://www.ycombinator.com/"https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/1-Gusto-Overview.png/" alt=\"Gusto Payroll Overview\" width=\"1950\" height=\"1070\" class=\"aligncenter size-full wp-image-1104909\" srcset=\"https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/1-Gusto-Overview.png 1950w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/1-Gusto-Overview-300x165.png 300w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/1-Gusto-Overview-1024x562.png 1024w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/1-Gusto-Overview-768x421.png 768w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/1-Gusto-Overview-1536x843.png 1536w\" sizes=\"(max-width: 1950px) 100vw, 1950px\" /></p>\n<p>Gusto knew that payroll was a product which had to work, because people depended on it. So some of the normal Silicon Valley approaches to building quickly, and fixing later, wouldn’t work. Gusto’s product needed to provide reliable, timely, and precise tax calculations, filings, and payments to earn the trust of customers. The team initially focused on a narrow segment: businesses in California (1) that did not offer benefits or other deductions, (2) whose employees did not mind getting paid four business days after the company ran payroll and, (3) only had salaried employees. The goal was to solve the basics of payroll first and then to expand to more segments. This focus proved to be very beneficial, since it helped the company build a more solid foundation, and validate that its product was indeed much easier to use, and loved by customers.</p>\n<p>The founders were their own first customers, only paying themselves after they were able to run their paychecks seamlessly through their software. It took a year to get to a public beta. One year after public launch, Gusto reached 1,500 customers. Today, Gusto is available nationwide and customers can onboard employees and run payroll in a matter of minutes. The company serves over 200,000 businesses, and they’ve made payroll much more efficient: 72% of customers spend five minutes or less to run payroll.</p>\n<p><img loading=\"lazy\" src=https://www.ycombinator.com/"https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/2-gusto-img-payroll-portal.png/" alt=\"Gusto's Payroll Portal\" width=\"2199\" height=\"1558\" class=\"aligncenter size-full wp-image-1104910\" srcset=\"https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/2-gusto-img-payroll-portal.png 2199w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/2-gusto-img-payroll-portal-300x213.png 300w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/2-gusto-img-payroll-portal-1024x726.png 1024w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/2-gusto-img-payroll-portal-768x544.png 768w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/2-gusto-img-payroll-portal-1536x1088.png 1536w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/2-gusto-img-payroll-portal-2048x1451.png 2048w\" sizes=\"(max-width: 2199px) 100vw, 2199px\" /></p>\n<p>With its software up and running, Gusto needed to figure out its go-to-market strategy. SMBs had historically been hard to reach. Incumbents relied primarily on sales teams, which Gusto suspected actually limited their reach among SMBs. Cloud software had the potential to transform this process. For the first time, businesses could reach and serve customers with an entirely online strategy. And on top of that, the Gusto team knew that time was precious for SMB owners. What they needed was a product that worked, which was accurate, powerful, and also simple and easy to use. Gusto believed this is what modern software should be all about: a product that made life easier for its users, not more stressful. Gusto leaned into an online referral and brand-based go-to-market strategy rather than building out a direct outbound sales force. If the product was truly great, the company believed customer love and word-of-mouth would power growth. In fact, it would need to: Given the lower annual contract values of SMBs, they needed a strong inbound engine to make the economics work. This was a risky bet, but it worked. Within the first three years of launching, Gusto was serving more than 20,000 SMBs, with growth largely coming from referrals and word-of-mouth. Customers loved the product and wanted to tell other business owners about it.</p>\n<h1>Act 2: All-in-one People Platform</h1>\n<p>Starting with payroll made sense for two reasons. First, every business needs it. Second, building payroll architecture requires collecting and structuring a lot of data (where employees live, name, email, start date, dependents, salary, etc.). Once in place, this structured data positioned Gusto for its second act: to leverage the payroll core, keep investing in it, but also expand around it a “people platform” that would help SMBs build great places to work.</p>\n<p>One of the main drivers of this thinking was a desire to bring to SMBs all of the benefits, resources, tools, and advantages big companies have historically had. Large companies have whole departments helping with HR, IT, benefits, and more, plus a wide variety of technologies and tools at their disposal. SMBs have historically been on their own. Gusto wanted to change that. And today, Gusto has expanded to provide a wide swath of functionality: (1) employee onboarding that helps manage identity across the different tools used by the business, (2) more accessible benefits, (3) access to tax credits, (4) financial optimization tools for employees, and more. With Gusto, SMB owners are able to spend more time running their businesses and less time on back-office work, while actually making their employees happier.</p>\n<p><img loading=\"lazy\" src=https://www.ycombinator.com/"https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/3-gusto-blog-img-2.png/" alt=\"Gusto - The People Platform\" width=\"2050\" height=\"1070\" class=\"aligncenter size-full wp-image-1104911\" srcset=\"https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/3-gusto-blog-img-2.png 2050w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/3-gusto-blog-img-2-300x157.png 300w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/3-gusto-blog-img-2-1024x534.png 1024w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/3-gusto-blog-img-2-768x401.png 768w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/3-gusto-blog-img-2-1536x802.png 1536w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/3-gusto-blog-img-2-2048x1069.png 2048w\" sizes=\"(max-width: 2050px) 100vw, 2050px\" /></p>\n<h3>People software for SMBs</h3>\n<p>Gusto began by making its product the central source of truth for hiring, onboarding, and employee communication. With Gusto, SMBs can create offer letters, complete onboarding checklists, and set-up software for new hires—traditionally manual and time-consuming processes. When a new employee signs on, Gusto tracks progress of offer signing, distributes forms and plans, and makes sure the employee has access to the software they need. After onboarding, Gusto enables time tracking, employee surveys, and distribution of the employee’s documents.</p>\n<p>Beyond massively reducing process inefficiency, Gusto has focused on customer delight permeating all aspects of its product. When a candidate receives an offer, the experience feels akin to a wedding invitation, versus the typical “check-the-box” paperwork. When a new hire joins, employees can post welcome messages on Gusto’s internal message board. On payday, employees receive a celebratory email, which the employer can add a personal message to. All of this transforms what was once a purely transactional experience to one that is more people centric, in which employees are treated as valued members of the company.</p>\n<p><img loading=\"lazy\" src=https://www.ycombinator.com/"https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/4-gusto-img-payday-email-e1630292881349.png/" alt=\"Gusto Payday Email\" width=\"750\" height=\"1074\" class=\"aligncenter size-full wp-image-1104912\" /></p>\n<p>On the employer side, customer delight manifests in saved time and helpful guidance. When it is time to run payroll, Gusto sends managers a reminder to sign forms, approve expenses, and initiate payroll. Each quarter, Gusto sends an email to employers summarizing employee changes and all the background tasks that have been completed automatically by Gusto, with no action needed from the employer. Gusto also integrates with expense and accounting tools, eliminating the manual work of recording payroll entries and approving expenses. And employers are able to use Gusto as a system of record for their employees, which means employees are easily able to access benefits and other employment-related information on their own even after leaving their company, all through the Gusto mobile app. All of this results in massive time savings for employers, allowing them to focus on actually running their business.</p>\n<p>Whereas incumbents designed their products to be reactive to customer needs, the Gusto product experience more closely resembles a human HR advisor, something SMBs typically do not have. This support system creates a relationship built on trust, where Gusto is valued as an opinionated partner rather than just another payroll tool. SMBs want a partner they can trust, that also provides great service and great technology; Gusto has strived to be great at both.</p>\n<h3>Improving access to health benefits</h3>\n<p>Providing health benefits to employees is costly, complicated, and time-consuming for SMBs. Traditionally, SMBs work with benefits brokers in a largely offline process. First, they have to find a broker. Then, they have to go through the tedium of gathering the business and employee information the broker needs. The broker then shares benefit options based on their specific carrier relationships, which are often limited and result in suboptimal and expensive options for SMBs. Once a plan is chosen, employers and brokers put together an enrollment program to drive adoption within the organization. There is then continuing overhead as employers work with brokers to manage renewals, new hires, and plan changes, often in a very manual fashion. Because of this complex process, basic benefits like health insurance are often too much for a small business to manage. Data suggest that only 56% of companies with fewer than 100 employees offer health benefits (versus 90% for 500+ employee businesses).<sup id=\"footnoteid5\"><a href=https://www.ycombinator.com/"#footnote5\">5</a></sup></p>\n<p>Gusto reduces all this friction. As a licensed broker with payroll data already, Gusto makes it possible for a business to buy health insurance in a few clicks, rather than having to resubmit the information over and over again. And if the customer wants to speak with someone, Gusto has licensed benefits advisors on staff. Gusto also lowers the cost of benefits. Traditionally, pricing varies significantly because different providers have different loss ratios. Gusto applies algorithms to thousands of health plans to help customers choose the most cost-effective and appropriate plans for their situation. And for employers who cannot afford small group insurance, Gusto offers QSEHRA, a health reimbursement account built into payroll that employers can contribute pre-tax dollars to every month. Long-term, we believe Gusto may even be able to use its scale to reduce insurance costs by creating its own health plans in partnership with insurance carriers, further lowering costs for SMBs.</p>\n<p>Gusto also enables customers to access government programs and benefits as they arise in real time. The best example of this happened during the COVID-19 lockdown. While small businesses were struggling, Gusto created a <a href=https://www.ycombinator.com/"https://covidresources.gusto.com//">COVID-19 resources</a> tool for its customers to take advantage of programs like the Payroll Protection Program (PPP). Gusto simplified complex forms and enabled customers to easily apply for PPP loans through their partners. With this program, Gusto helped generate billions of dollars in assistance for its customers.</p>\n<p><img loading=\"lazy\" src=https://www.ycombinator.com/"https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/5-gusto-img-benefits-experience.png/" alt=\"Gusto's Benefits Experience\" width=\"1832\" height=\"1954\" class=\"aligncenter size-full wp-image-1104913\" srcset=\"https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/5-gusto-img-benefits-experience.png 1832w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/5-gusto-img-benefits-experience-281x300.png 281w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/5-gusto-img-benefits-experience-960x1024.png 960w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/5-gusto-img-benefits-experience-768x819.png 768w, https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/5-gusto-img-benefits-experience-1440x1536.png 1440w\" sizes=\"(max-width: 1832px) 100vw, 1832px\" /></p>\n<h3>Helping employees optimize their finances</h3>\n<p>Gusto has endeavored to treat the employee as an equal stakeholder from day one. And in the past few years, the company has been making meaningful investments to help employees with their personal finances. Payroll is the inception of one’s income. Gusto had the simple insight that, if they could make personal finance choices (like saving) much simpler and easier, then people would make these choices more often. Gusto first launched <a href=https://www.ycombinator.com/"https://gusto.com/product/cashout/">Cashout, a product to help employees avoid payday loans and high-interest credit card debt by giving them early access to paychecks at no cost. In a tight labor market, companies have turned to this type of benefit to attract and retain employees, and the number of businesses with employees enrolled in Cashout has more than doubled since January 2021. Cashout has helped 73% of users prevent bank overdrafts, and 52% of employees say having access to Cashout would impact whether they accept a job or not.</p>\n<p>But Gusto’s broader goal is for employees to not need Cashout in the first place. If an individual had savings in place, then during an emergency, they would have the funds they need already. To help employees with savings, banking, and more, Gusto introduced <a href=https://www.ycombinator.com/"https://gusto.com/wallet/">Gusto Wallet</a> in 2020, a free banking app that lets employees put their paycheck, banking, savings, and emergency funds in one place. Employees are able to put aside part of their paycheck into savings, creating a rainy day fund for emergencies. Plus, they’re able to connect payroll & banking in one holistic experience. Looking ahead, Gusto is well-positioned to continue launching new employee services with seamless integration processes. These products are a win-win-win: Employers get value with free benefits for employees, employees have access to powerful spending and savings tools, and Gusto further differentiates its product.</p>\n<p><img loading=\"lazy\" src=https://www.ycombinator.com/"https://ghost.prod.ycinside.com/content/images/wordpress/2021/08/6-gusto-img-wallet-e1630292853481.png/" alt=\"Gusto Wallet\" width=\"750\" height=\"1074\" class=\"aligncenter size-full wp-image-1104914\" /></p>\n<h3>A people platform powered by people</h3>\n<p>Gusto’s approach to customer service and product has led to levels of customer love previously unheard of in the SMB software space. In the decade since its launch, Gusto has become a beloved nationwide brand, helping 200,000+ SMBs across the US (over 3% market share<sup id=\"footnoteid6\"><a href=https://www.ycombinator.com/"#footnote6\">6</a></sup>) process hundreds of billion dollars of payroll, all while maintaining an NPS that is typically only seen among popular consumer companies. Its significant market share and growth trajectory signal to us that Gusto is already filling a long-standing gap in the SMB landscape. We believe that Gusto will continue to grow and compound for decades to come, as the platform expands and gains a wider reputation as a better and more cost-effective alternative to incumbents.</p>\n<h1>Act 3: New Ways to Empower Teams</h1>\n<p>Looking ahead, we believe Gusto has two major opportunities to build on top of the solid foundation they’ve created.</p>\n<p>The first is to simply build more products for businesses and their employees. Because Gusto sits at the intersection of employees and employers, it is in a prime position to launch new products for both parties. Gusto can keep making their lives easier, help employers run better businesses, and help employees accomplish their work goals. On the employee side, Gusto could become a primary bank account, seamlessly setting up direct deposits. In time, Gusto could layer on investment products and even peer-to-peer payment tools. On the employer side, Gusto is positioned to help solve many other pain points, including further streamlining government compliance and reporting, making healthcare even more accessible, making business financials easier, and more.</p>\n<p>In 2021, Gusto expanded into new services through acquisitions. Gusto recently acquired <a href=https://www.ycombinator.com/"https://gusto.com/company-news/welcoming-ardius-to-gusto/">Ardius, an AI-powered tax credit solution, to help SMBs access valuable R&D tax credits that historically have been too cumbersome to apply for. Because Gusto already manages its customers’ payroll documentation, it’s now infinitely easier for SMBs to access these credits and improve their cash flow. Gusto also acquired <a href=https://www.ycombinator.com/"https://gusto.com/company-news/welcoming-symmetry-to-gusto/">Symmetry, an infrastructure company that builds APIs for payroll tax calculations. Together, Symmetry and Gusto will be able to make advances that benefit the entire payroll industry. For example, they could develop an early alert system for tax code changes, notifying business owners when state or local minimum wage requirements change, and ensuring employees complete the required withholding forms.</p>\n<p>The second major opportunity we see is in embedded services. Gusto recently launched <a href=https://www.ycombinator.com/"https://gusto.com/company-news/introducing-gusto-embedded-payroll/">Gusto Embedded Payroll</a> to allow business-to-business (B2B) software companies to offer payroll capabilities to their own customers via APIs. For example, Squire (YC S16), a company that builds software and tools for barbershops, will offer payroll features in its own app using Gusto’s functionality. This provides a better experience for barbershops, generates more revenue for Squire, and extends Gusto’s payroll platform beyond their direct customers. Embedded services not only unlocks new opportunities to serve SMBs within vertical SaaS, fintech, and business operations, but it also exposes millions of new businesses to modern payroll. And as we’ve seen, payroll is just the beginning. Gusto is working to provide developers with APIs to embed its suite of people products into their own platforms, as a full-fledged Infrastructure-as-a-Service (IaaS) solution.</p>\n<h1>Conclusion</h1>\n<p><em>“Software is better at following rules but people make the experience incredible.”</em></p>\n<p>This quote from Josh Reeves embodies the ethos of Gusto. The company’s powerful software has modernized the way SMBs run and empowered employees to be in the driver’s seat of their finances, but the real key to its success has been the insight that people are the foundation of any business. People are what make SMBs special. With Gusto, SMBs in the US and the people that work in them are positioned better than ever to succeed.</p>\n<p><em>Thank you to Mia Mabanta and Chloe Gordon for reading multiple drafts of this essay, and to Zain Ali for designing and editing the graphics.</em></p>\n<hr />\n<p><sup><b id=\"footnote1\">1</b></sup> US Census: Firms and Establishments by State, Industry (2018; released May 2021) <a href=https://www.ycombinator.com/"#footnoteid1\">↩</a><br />\n<sup><b id=\"footnote2\">2</b></sup> 2018 Small Business Taxation Survey <a href=https://www.ycombinator.com/"#footnoteid2\">↩</a><br />\n<sup><b id=\"footnote3\">3</b></sup> 2018 Small Business Taxation Survey <a href=https://www.ycombinator.com/"#footnoteid3\">↩</a><br />\n<sup><b id=\"footnote4\">4</b></sup> 2018 Internal Revenue Services estimates <a href=https://www.ycombinator.com/"#footnoteid4\">↩</a><br />\n<sup><b id=\"footnote5\">5</b></sup> Bureau of Labor Statistics: Employee Benefits in the United States (March 2020). <a href=https://www.ycombinator.com/"#footnoteid5\">↩</a><br />\n<sup><b id=\"footnote6\">6</b></sup> There are approximately 6 million employers in the US. <a href=https://www.ycombinator.com/"#footnoteid6\">↩</a></p>\n<!--kg-card-end: html-->","comment_id":"1104906","feature_image":"/blog/content/images/2022/02/3-gusto-blog-img-2.png","featured":false,"visibility":"public","email_recipient_filter":"none","created_at":"2021-08-30T03:00:01.000-07:00","updated_at":"2022-10-17T12:17:00.000-07:00","published_at":"2021-08-30T03:00:01.000-07:00","custom_excerpt":null,"codeinjection_head":null,"codeinjection_foot":null,"custom_template":null,"canonical_url":null,"authors":[{"id":"61fe29e3c7139e0001a7107b","name":"Anu Hariharan","slug":"anu-hariharan","profile_image":"/blog/content/images/2022/02/Anu.png","cover_image":null,"bio":"Anu is a Managing Director & Partner at YC Continuity. Previously, Anu was a Partner at a16z, where she worked actively with the management teams of companies including Airbnb, Instacart, and Medium.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/anu-hariharan/"},{"id":"61fe29e3c7139e0001a710b2","name":"Nic Dardenne","slug":"nic-dardenne","profile_image":"/blog/content/images/2022/02/Nic.jpg","cover_image":null,"bio":"Nic is a principal at YC Continuity. Nic has helped support the teams at Brex, Convoy, Faire, Groww, Monzo, Rappi, Segment, Snapdocs, and Vouch. Before YC, Nic worked as an analyst at Morgan Stanley.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/nic-dardenne/"}],"tags":[{"id":"61fe29efc7139e0001a7116d","name":"Essay","slug":"essay","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/essay/"},{"id":"61fe29efc7139e0001a71170","name":"Startups","slug":"startups","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/startups/"},{"id":"61fe29efc7139e0001a71182","name":"#ycc","slug":"hash-ycc","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"61fe29efc7139e0001a711b7","name":"#24","slug":"hash-24","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"}],"primary_author":{"id":"61fe29e3c7139e0001a7107b","name":"Anu Hariharan","slug":"anu-hariharan","profile_image":"https://ghost.prod.ycinside.com/content/images/2022/02/Anu.png","cover_image":null,"bio":"Anu is a Managing Director & Partner at YC Continuity. Previously, Anu was a Partner at a16z, where she worked actively with the management teams of companies including Airbnb, Instacart, and Medium.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/anu-hariharan/"},"primary_tag":{"id":"61fe29efc7139e0001a7116d","name":"Essay","slug":"essay","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/essay/"},"url":"https://ghost.prod.ycinside.com/gusto-the-people-platform-for-smbs/","excerpt":"Historically, there has been an undeniable gap in business services in the US.There are nearly six million small and medium businesses (SMBs) in the country,employing 43 million people.1 But unlike their larger counterparts, SMBs havebeen ignored by service providers, who have deemed the cost of reaching andserving them too high to warrant the effort. As a result, SMBs have been forcedto cobble together off-the-shelf products, spreadsheets, and manual work to runtheir operations.","reading_time":14,"access":true,"og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"email_subject":null,"frontmatter":null,"feature_image_alt":null,"feature_image_caption":null},{"id":"61fe29f1c7139e0001a71be7","uuid":"dfe1c037-74e0-460c-96ee-cc20ff699ff9","title":"Brex: The Future of Business Finance and Cash Management","slug":"brex-the-future-of-business-banking-and-cash-management","html":"<!--kg-card-begin: html--><p>When Henrique Dubugras and Pedro Franceschi joined the YC W17 batch with an idea for a VR startup, they quickly encountered a problem. They had applied for a business credit card to help fund software and other expenses and were denied. Business credit is traditionally underwritten based on the founders’ FICO scores. As international founders with less than a month of credit history, their chances of getting approved were slim to none, despite having $125K in the bank.</p>\n<p>It wasn’t just them. They discovered that, while early startup founders had access to high-fidelity payments products like <a href=https://www.ycombinator.com/"http://stripe.com/">Stripe (YC S09) right from the get-go, getting access to basic cash management and credit products was a terrible experience for everyone. Even with $125K from YC and $1–2M in venture funding, a startup’s credit limit is still likely to tap out at $20K from an incumbent creditor—which is not nearly enough to cover software, marketing, and other expenses. Cards are particularly a must have for young companies because large vendors don’t often accept ACH and other forms of alternative payment from early startups. In practice, this leads to founders resorting to using their personal credit cards for SaaS subscriptions or digital marketing, and filing reimbursements regularly.</p>\n<p>Stripe also set a great example in how they transformed the internet’s payment infrastructure. Stripe’s launch in 2009 made it possible for startups to easily collect payments online via developer-friendly APIs. Over time, Stripe has expanded to support more business models (e.g., ecommerce, SaaS, marketplaces) and verticals.</p>\n<p>While products like Stripe and Square have dramatically pushed business-to-consumer (B2C) transactions to credit cards, business-to-business (B2B) card penetration has remained stubbornly low. The US B2B payments market is three times the size of the B2C market—yet B2B digital payments penetration is 36%, half as much as B2C (67%). B2B credit card adoption is especially low, accounting for only 4% of the market.<sup id=\"footnoteid1\"><a href=https://www.ycombinator.com/"#footnote1\">1</a></sup></p>\n<p><img src=https://www.ycombinator.com/"https://ghost.prod.ycinside.com/content/images/wordpress/2021/04/brex-tpv-bar-graphic-01.jpg/" alt=\"US Payments Market\" /></p>\n<p>The extremely low penetration of credit cards in the B2B space is a historical remnant of the industry. Checks remain the most popular payments channel because, in addition to being simple and virtually free to use, they’ve been around the longest. ACH came next in the 1970s and now makes up half the payments volume as checks (mostly in recurring payments such as payroll and billing).</p>\n<p>Meanwhile, card adoption is only 4% not for a lack of demand, but because of the significant friction in the accessibility, onboarding, and utility of the product. Most banks and card providers ask for excessive documentation, take 3–5 days to onboard customers, and require a personal guarantee from business founders and owner-operators. Even then, the credit limits they offer are minimal, since they’re being underwritten on the personal credit history of the founder and not the health of the business. And a further obstacle: the walled garden of most enterprise resource planning (ERP) systems makes it difficult for new payment solutions to readily integrate with a company’s accounting software, adding administrative cost to reconciliations and making the total cost of introducing a new payment system incredibly high for small businesses.</p>\n<p>To address this massive underappreciated market opportunity (not to mention a personal pain point), Henrique and Pedro pivoted and built Brex. They had the benefit of having previously founded a Stripe-like payments company as teenagers in Brazil. They had scaled that company to $1B+ in annual payments volume, then sold it. Having already developed an understanding of the initial card infrastructure stack needed to build Brex, they were able to move fast and launched their first product within six months.</p>\n<p>The initial Brex product was a simple 30-day charge card for startups with credit limits based on cash balance. The value proposition was clear: Founders didn’t have to personally guarantee, it took less than 24 hours to get approved, and businesses could access 10–20x higher credit limits since underwriting was based on cash balance. They further differentiated the product with several intuitive features. Brex gave startup founders a daily view into the month’s cumulative expenses (vs. incumbent offerings which only offered end-of-month reconciliation). They made it 10x easier to file expenses: whenever an employee used their Brex Card to pay for something, they instantly got a text that let them immediately send in the receipt (vs. having to deal with saving receipts and filing them all at the end of the month). Lastly, they designed a rewards program for startups, offering customers things like rewards on SaaS spend and discounts on AWS and Zoom.</p>\n<p>Brex’s product-market fit was instantaneous, and the product has spread like wildfire among venture-backed startups. Within five months of launching, Brex grew from 100 to 1,000 customers. In the less than three years since launching, they’ve scaled to over 20,000 customers (including 60% of all YC companies).</p>\n<p>Henrique and Pedro’s vision for Brex isn’t just to issue credit cards to startups—it’s to become the financial operating system for growing businesses. We believe that Brex’s experience represents the next great shift in global B2B financial transactions.</p>\n<h2>The Beginning: Removing friction to unlock demand</h2>\n<p>Early on, Brex understood that removing the friction of financial products could meaningfully differentiate them from the status quo. Brex’s initial insight was simple: “You should be able to sign up for a credit card and other financial services as easily as you can set up an email address—in minutes, all online.” Once they began to onboard customers, Brex found that the demand for seamless finance was even bigger than they had initially imagined.</p>\n<p>To provide the modern and seamless service they envisioned, Brex built a risk assessment system that was fundamentally different from traditional credit card underwriting. They removed the paper-based back-and-forth of traditional KYC<sup id=\"footnoteid2\"><a href=https://www.ycombinator.com/"#footnote2\">2</a></sup> processes and built systems that could collect and verify critical business information (like beneficial ownership) in seconds. They then built their own ledger that used real-time cash, operating, and transaction data to underwrite customers to credit limits with multiple levels of authorization. Incumbent underwriters rely on point-in-time data and must build confidence in customers over long periods of time. Brex’s digital approach enabled them to instantly onboard customers with 10-20x higher credit limits than incumbents were able to offer. These methods have proven to be highly efficient: Brex’s credit losses have been lower than those of Amex and Silicon Valley Bank, even when including the impact of COVID-19.</p>\n<p>Demand for frictionless financial services soon spread far beyond venture-backed startups. Every month, more than 10,000 businesses across the country were signing up. But because their underwriting system was built for tech startups, Brex had been turning away more than 80% of those potential customers. In late 2020, Brex decided to retool their system to serve more customer segments.</p>\n<p>With the average business in mind, Brex launched a new risk system that could instantly onboard any legitimate business to a cash management account and a same-day charge card (a debit card-like product). This change enabled Brex to grow new monthly customers tenfold, and they were able to maintain instant same-day approvals for 80% of those customers. In the first quarter of 2021, Brex onboarded more customers than it did in the entire history of the company and. Today, more than 70% of new customers are traditional small and medium businesses.</p>\n<h2>Today: Scaling from cards to cash management and financial software tools</h2>\n<p>The next act for Brex was to launch complementary financial and software products beyond credit cards. Last year, they launched a service that transformed the trajectory of their platform: Brex Cash. Brex Cash was imagined as a bank account replacement product that would let Brex serve companies even before they qualify for credit. It was also a way for customers to send checks, ACH, and wire payments to vendors and third parties that didn’t accept credit cards (remember, 96% of B2B payments in the US are non-card).<sup id=\"footnoteid3\"><a href=https://www.ycombinator.com/"#footnote3\">3</a></sup></p>\n<p>But Brex Cash is not just an add-on product. It is a deeply integrated solution that reimagines and streamlines workflows for various forms of payments.</p>\n<p>Brex designed Brex Cash to be the center of a company’s financial operations, rather than an account used solely for financial services. This meant that the product had to be intuitive and designed for daily use. Brex removed all fees on ACH and wires, improved payment speed and user flows (Brex’s payment initiation is 40–50x faster than competitors’), and built in utility beyond financial services. For example, they’ve drastically reduced customers’ accounting workloads by integrating Cash into third-party accounting systems. These integrations have made it possible for SMBs like <a href=https://www.ycombinator.com/"https://www.op2labs.com//">OP2 to save the 20–30 hours a week they previously spent downloading bank statements and doing manual reconciliation.</p>\n<p>Today, Brex has more than 10,000 customers ranging from small venture-backed startups and traditional SMBs to large growth-stage businesses using both Brex Cash and the Brex Card. In our view, Cash is the foundational product that is transitioning Brex from a card-issuing company to an all-in-one finance operations platform.</p>\n<p>As Brex has scaled, so have their customers. Many of their early startup customers have grown into large organizations whose needs have evolved past simple credit cards. To keep up with customers, Brex has moved quickly to shift from a team-centric product to an enterprise product. They’ve created department- and category-level tracking tools where leadership and finance teams can better understand organizational spend against budgets. Companies can now also use Brex’s virtual cards infrastructure to issue cards to specific organizations and employees rather than dealing with individual reimbursements. This alone translates to hours of time saved for employees and finance teams. Today, large startups like <a href=https://www.ycombinator.com/"https://scale.com//">Scale AI</a> (YC S16), <a href=https://www.ycombinator.com/"https://www.rippling.com//">Rippling (YC W17), <a href=https://www.ycombinator.com/"https://www.rappi.com//">Rappi (YC W16) and <a href=https://www.ycombinator.com/"https://www.flexport.com/?utm_source=google&utm_medium=paid-search&utm_term=flexport&utm_content=402161566078&utm_campaign=us-flexport-trademarks&_bt=402161566078&_bk=flexport&_bm=e&_bn=g&_bg=84747732606&campaign_id=316515561&gclid=CjwKCAjwg4-EBhBwEiwAzYAlspI018GdhXf142JjoTNC2OuR0GaVHDvKtchnW40hGNhIEGVuPMlc3RoCGX4QAvD_BwE\%22>Flexport (YC W14), among many others, use Brex as a central tool for managing finances.</p>\n<h2>The future: All-in-one finance</h2>\n<p>With more and more companies using Brex Cash, Brex is on its way to becoming a first of its kind all-in-one finance platform. Historically, financial operations software and financial products have existed separately. The incumbent system involves three key “stacks.” The first stack is the payments infrastructure (checks, ACH, and card networks) that processes transactions. The second is the access providers to the underlying infrastructure—institutions like Amex and Chase that manage the storage and movement of funds. Finally there is the value-added services stack, made up of products that handle administrative back-office tasks (such as Intuit, Bill.com, and Concur).</p>\n<p><img src=https://www.ycombinator.com/"https://ghost.prod.ycinside.com/content/images/wordpress/2021/04/YC-Brex-AIO-3Stacks.png/" alt=\"The 3 Stacks of Financial Services\" /></p>\n<p>Because of how this system is designed, the average SMB uses at least six different financial services and software providers to manage its business. A typical ecommerce company may use Chase for storing capital, American Express for travel and software spend, Bill.com to manage payables, Expensify to manage employee spend, Quickbooks for accounting, Shopify or Stripe for accepting payments, and a third-party lender for a longer-term working capital financing product. While all these solutions do have the ability to talk to each other, there is no single entity that has a holistic view of the business’ financial operations.</p>\n<p><img src=https://www.ycombinator.com/"https://ghost.prod.ycinside.com/content/images/wordpress/2021/05/brex-operating-system.png/" alt=\"Today's Financial Operating System\" /></p>\n<p>Brex is changing the landscape by combining financial products and software into a single platform. The company has spent the past two years building its card processing and cash management infrastructure, which in turn will power its software (e.g., Expense Management, Bill Pay). Enabled by its financial infrastructure, Brex is building the “financial operating system” for growing businesses, enabling them to spend and track payments across all mediums.</p>\n<p><img src=https://www.ycombinator.com/"https://ghost.prod.ycinside.com/content/images/wordpress/2021/04/YC-Brex-AIO-5.png/" alt=\"Brex's Financial Operating System\" /></p>\n<p>We are already seeing how integrating the financial stack is enabling greater access to financial resources and only expect these resources to improve as Brex moves closer to a true all-in-one finance platform.</p>\n<p>By owning both software and financial infrastructure, Brex is able to:</p>\n<p><strong>(1) Leverage customer data to offer better financial products than competitors:</strong> When customers make the free Brex Cash account their primary operating account, Brex gains full visibility of their customers’ financial health. Currently, Brex uses this data to predict estimated runway and dynamically sets credit limits that can be up to 10–20x more than what legacy competitors offer. <a href=https://www.ycombinator.com/"https://datrics.ai//">Datrics (YC W21) uses both Brex Cash and Card for this reason. In the future, Brex could identify startups and SMBs that serve “safer” customers (i.e., large enterprises) and leverage repayment data and relationship history to offer bill discounting/invoice factoring and other credit products.</p>\n<p><strong>(2) Drive deep value for customers via software:</strong> The payment workflow integrations that come with the Spend Management software effectively deliver a product that is not just a system-of-record but also a system-of-engagement for customers. This drives immense value not just through lower fees but cost savings and more efficient operations across the board. Back-office administrative teams spend significant hours in manual processes like standardizing invoices, matching invoices to purchase orders, managing billing information for several vendors, payment approvals, and accounts reconciliation/reporting. By integrating the financial stack, Brex can automate these processes, saving companies time and money.</p>\n<p><strong>(3) Build unique financial products:</strong> Building on its positioning as both a software and financial services provider, Brex can offer financial services products that are not readily available from incumbents. There is no better example of this than Instant Payouts, which launched in Q4 of 2020. An ecommerce merchant can instantly settle funds through the click of a button in their Brex dashboard, instead of waiting two weeks for the revenue to be distributed to their account. Funds are instantly disbursed in exchange for a fee that can be paid with Brex Card points. This is incredibly valuable because it enables ecommerce sellers to smooth out their cash flow and reinvest it in growth regardless of the selling platform. While the customer-facing product is simple, the backend infrastructure is sophisticated, integrating Brex Card, Cash and underwriting stacks.</p>\n<p><strong>(4) Lower the cost for customers:</strong> As a financial services provider and a software company, Brex is disrupting existing pricing models of point solutions in both layers. By monetizing customers through card interchange fees, Brex is able to price software far lower than a pure SaaS competitor can charge. An SMB with 20 employees may have to pay ~$4,200 per year for Expensify, Bill.com, and Quickbooks. Brex customers can pay a tenth of that in fees and get all of their spend data in a single place. Brex can choose to give even more value back to customers by making any of its products loss leaders to encourage new transactions on the platform. For example, Brex does not charge fees on any bank or wire transfers today, an unconventional practice among incumbents.</p>\n<p><strong>(5) Launch customer-centric products faster:</strong> By limiting reliance on third parties, Brex can build and launch products faster. In less than two years, the company has been able to quickly expand from a single-product company to a multiproduct company (Card, Cash, Instant Payouts, Bill Pay, and Expense Management) because they own everything from the general ledger to the credit box and can quickly build on their own infrastructure.</p>\n<p><img src=https://www.ycombinator.com/"https://ghost.prod.ycinside.com/content/images/wordpress/2021/04/brex-timeline-graphic-01.jpg/" alt=\"Brex timeline\" /></p>\n<p>As Brex scales, its data-driven underwriting algorithm will benefit immensely from an expanding customer base that feeds back into the company’s models. Over time, this should yield a lower-delinquency credit book. On the flip side, the diversification of the credit book and seasoning across economic periods should yield cheaper cost of capital over time, which will translate to higher margins for Brex and/or lower pricing for its customers. Brex is also among the first fintech companies (and the first in a B2B use case) that has filed for an industrial loan charter, which will allow Brex Cash to transform into a full-fledged “business bank.” With the ability to lend using Brex Cash customers’ deposits, Brex will be able to provide loans and credit cards at a lower cost of capital.</p>\n<p>The financial upsides of an integrated system are significant. The overall infrastructure and ease of use create more capital for both small and growing businesses. Digitizing B2B finances can entirely change the trajectory of a business. <a href=https://www.ycombinator.com/"https://www.op2labs.com//">OP2 uses both Brex Cash and Card because the combination enables credit limits three times higher than the next competitor, which has allowed the company to meaningfully grow. We see the future of Brex as existing hand-in-hand with the future of growing businesses.</p>\n<h2>Conclusion: The inevitability of digital B2B payments</h2>\n<p>In the past decade, we’ve seen the emergence of large players that have reduced friction and enabled digitization of consumer-to-business (C2B) payments by helping both consumers pay digitally (Cash App and PayPal) and helping merchants accept digital payments (Square and Stripe). Meanwhile, B2B payments account for nearly 3x the volume of C2B and the electronic payment penetration is fractional in comparison. The digitization of B2B payments is inevitable in the decades to come.</p>\n<p>There is no one way to address this problem, and the market has a spectrum of use cases that need to be addressed. This is also not a zero-sum game; we believe the $25T B2B payments market is large enough to support several companies. Brex is only one of the companies that has revealed the underlying demand and it has only grown more desperate in COVID. In a recent Mastercard study of payment type usage during the pandemic, online card payments saw the greatest increase (+60%) while cash (-34%) and checks (-24%) decreased the most. Legacy players’ archaic infrastructure and high-fee models have created a natural ceiling for how many businesses they can service. Just like consumer payments adoption, we believe that the majority of digital payment adoption will be led by Brex and other modern fintech companies, such as <a href=https://www.ycombinator.com/"https://www.moderntreasury.com/?utm_medium=search&utm_source=Google&utm_campaign=Google-brand-2019-02-11&utm_content=search-brand&utm_term=modern%20treasury&utm_campaign=Google-brand-2019-02-11&utm_source=adwords&utm_medium=ppc&hsa_acc=9452648776&hsa_cam=1702893340&hsa_grp=69100369840&hsa_ad=337065672658&hsa_src=g&hsa_tgt=kwd-633654608865&hsa_kw=modern%20treasury&hsa_mt=e&hsa_net=adwords&hsa_ver=3&gclid=CjwKCAjwg4-EBhBwEiwAzYAlspc-ch4IBRzFtcMi0y6SkvdrmGeCqnsqKIet0xRgaAolG0-SOU4xghoCRoEQAvD_BwE\%22>Modern Treasury</a> (YC S18) and <a href=https://www.ycombinator.com/"https://routable.com//">Routable (YC S17). We are excited about the next decade of B2B payments and believe many new multibillion-dollar businesses will emerge.</p>\n<p><em>Thank you to the Brex team, Mia Mabanta, and Chloe Gordon for reading multiple drafts of this essay, and to Zain Ali for designing the graphics.</em></p>\n<h2>Notes</h2>\n<p><b id=\"footnote1\">1.</b> Mastercard, SunTrust – Electronic B2B Payments: The Next Frontier <a href=https://www.ycombinator.com/"#footnoteid1\">↩</a><br />\n<b id=\"footnote2\">2.</b> Know-Your-Customer, a standard customer identity verification process <a href=https://www.ycombinator.com/"#footnoteid2\">↩</a><br />\n<b id=\"footnote3\">3.</b> Mastercard, SunTrust – Electronic B2B Payments: The Next Frontier <a href=https://www.ycombinator.com/"#footnoteid3\">↩</a></p>\n<!--kg-card-end: html-->","comment_id":"1104798","feature_image":"/blog/content/images/2022/02/brex-timeline-graphic-01.jpg","featured":false,"visibility":"public","email_recipient_filter":"none","created_at":"2021-04-25T23:30:26.000-07:00","updated_at":"2022-10-17T12:22:05.000-07:00","published_at":"2021-04-25T23:30:26.000-07:00","custom_excerpt":null,"codeinjection_head":null,"codeinjection_foot":null,"custom_template":null,"canonical_url":null,"authors":[{"id":"61fe29e3c7139e0001a7107b","name":"Anu Hariharan","slug":"anu-hariharan","profile_image":"/blog/content/images/2022/02/Anu.png","cover_image":null,"bio":"Anu is a Managing Director & Partner at YC Continuity. Previously, Anu was a Partner at a16z, where she worked actively with the management teams of companies including Airbnb, Instacart, and Medium.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/anu-hariharan/"},{"id":"61fe29e3c7139e0001a710b2","name":"Nic Dardenne","slug":"nic-dardenne","profile_image":"/blog/content/images/2022/02/Nic.jpg","cover_image":null,"bio":"Nic is a principal at YC Continuity. Nic has helped support the teams at Brex, Convoy, Faire, Groww, Monzo, Rappi, Segment, Snapdocs, and Vouch. Before YC, Nic worked as an analyst at Morgan Stanley.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/nic-dardenne/"}],"tags":[{"id":"61fe29efc7139e0001a7116d","name":"Essay","slug":"essay","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/essay/"},{"id":"61fe29efc7139e0001a71170","name":"Startups","slug":"startups","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/startups/"},{"id":"61fe29efc7139e0001a711b8","name":"#1556","slug":"hash-1556","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"}],"primary_author":{"id":"61fe29e3c7139e0001a7107b","name":"Anu Hariharan","slug":"anu-hariharan","profile_image":"https://ghost.prod.ycinside.com/content/images/2022/02/Anu.png","cover_image":null,"bio":"Anu is a Managing Director & Partner at YC Continuity. Previously, Anu was a Partner at a16z, where she worked actively with the management teams of companies including Airbnb, Instacart, and Medium.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/anu-hariharan/"},"primary_tag":{"id":"61fe29efc7139e0001a7116d","name":"Essay","slug":"essay","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/essay/"},"url":"https://ghost.prod.ycinside.com/brex-the-future-of-business-banking-and-cash-management/","excerpt":"When Henrique Dubugras and Pedro Franceschi joined the YC W17 batch with an ideafor a VR startup, they quickly encountered a problem. They had applied for abusiness credit card to help fund software and other expenses and were denied.Business credit is traditionally underwritten based on the founders’ FICOscores. As international founders with less than a month of credit history,their chances of getting approved were slim to none, despite having $125K in thebank.It wasn’t just them.","reading_time":12,"access":true,"og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"email_subject":null,"frontmatter":null,"feature_image_alt":null,"feature_image_caption":null}],"filter":"By Nic Dardenne","featured":null,"pagination":{"page":1,"limit":10,"pages":1,"total":3,"next":null,"prev":null}},"url":"/blog/author/nic-dardenne","version":null,"rails_context":{"railsEnv":"production","inMailer":false,"i18nLocale":"en","i18nDefaultLocale":"en","href":"https://www.ycombinator.com/blog/author/nic-dardenne","location":"/blog/author/nic-dardenne","scheme":"https","host":"www.ycombinator.com","port":null,"pathname":"/blog/author/nic-dardenne","search":null,"httpAcceptLanguage":"en, *","applyBatchLong":"Winter 2024","applyBatchShort":"W2024","applyDeadlineShort":"October 13","ycdcRetroMode":true,"currentUser":null,"serverSide":true},"id":"ycdc_new/pages/BlogList-react-component-6c4f67ae-740c-4129-a6bc-99cc2e2465bc","server_side":true}" data-reactroot="">