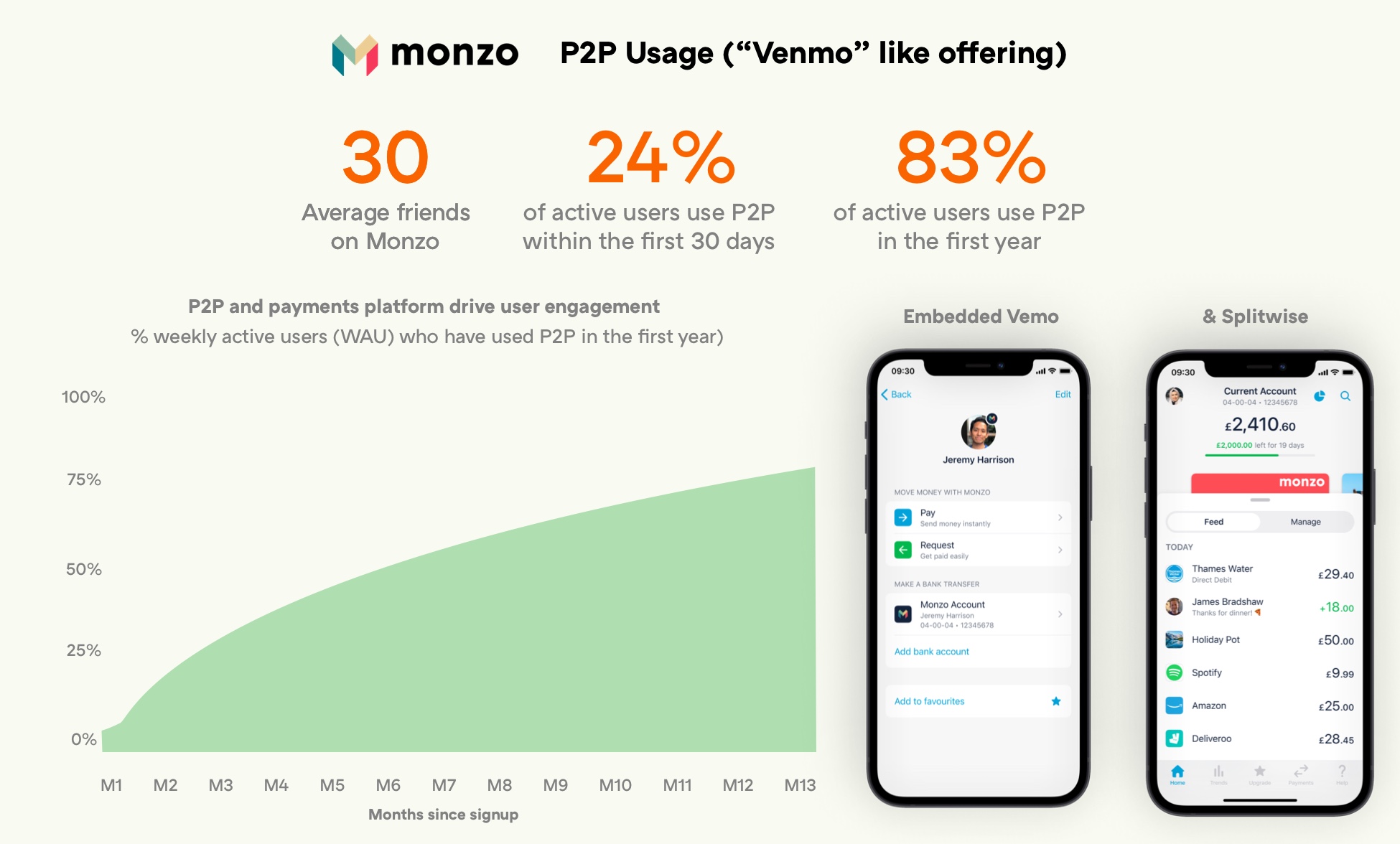

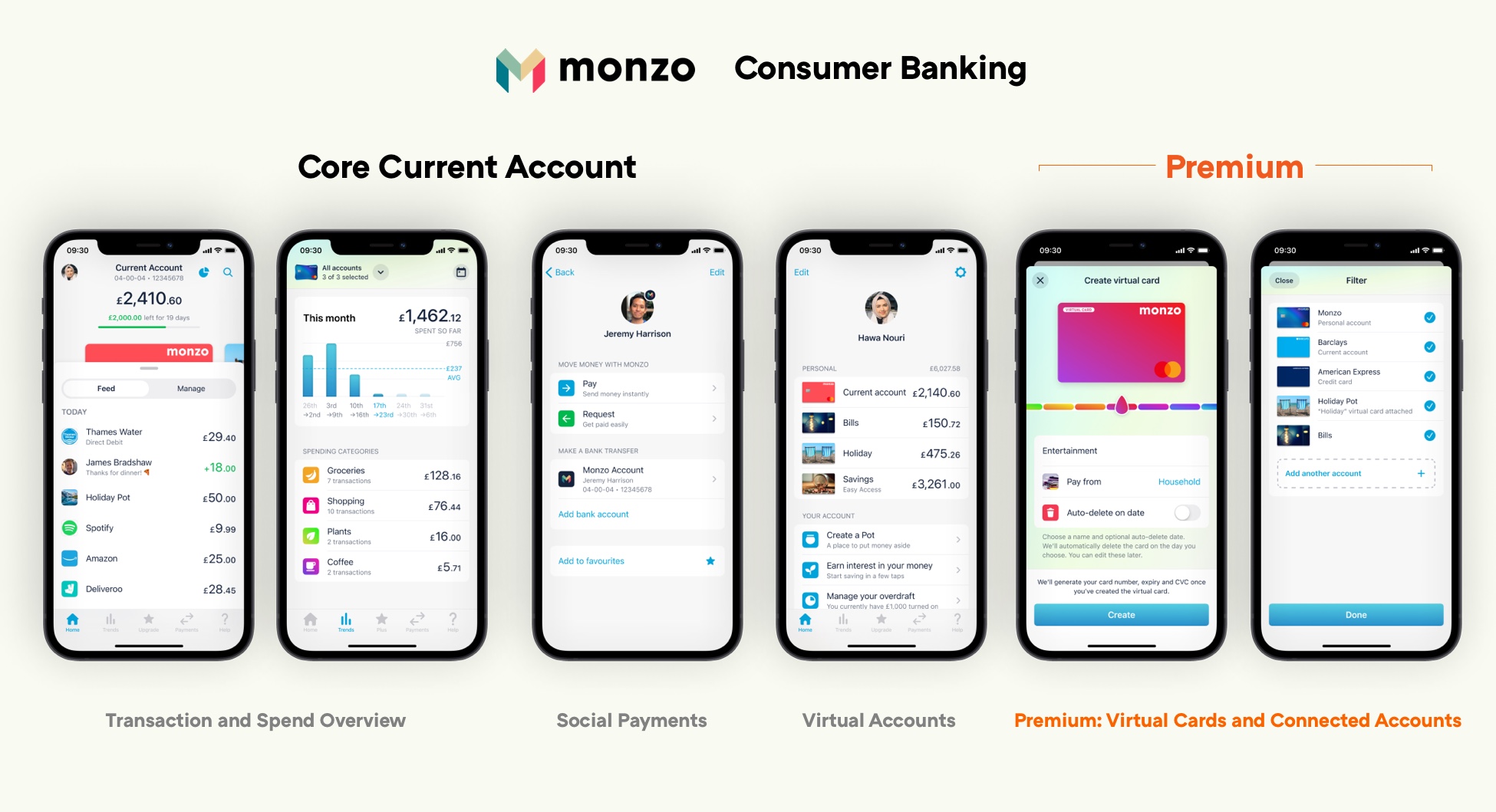

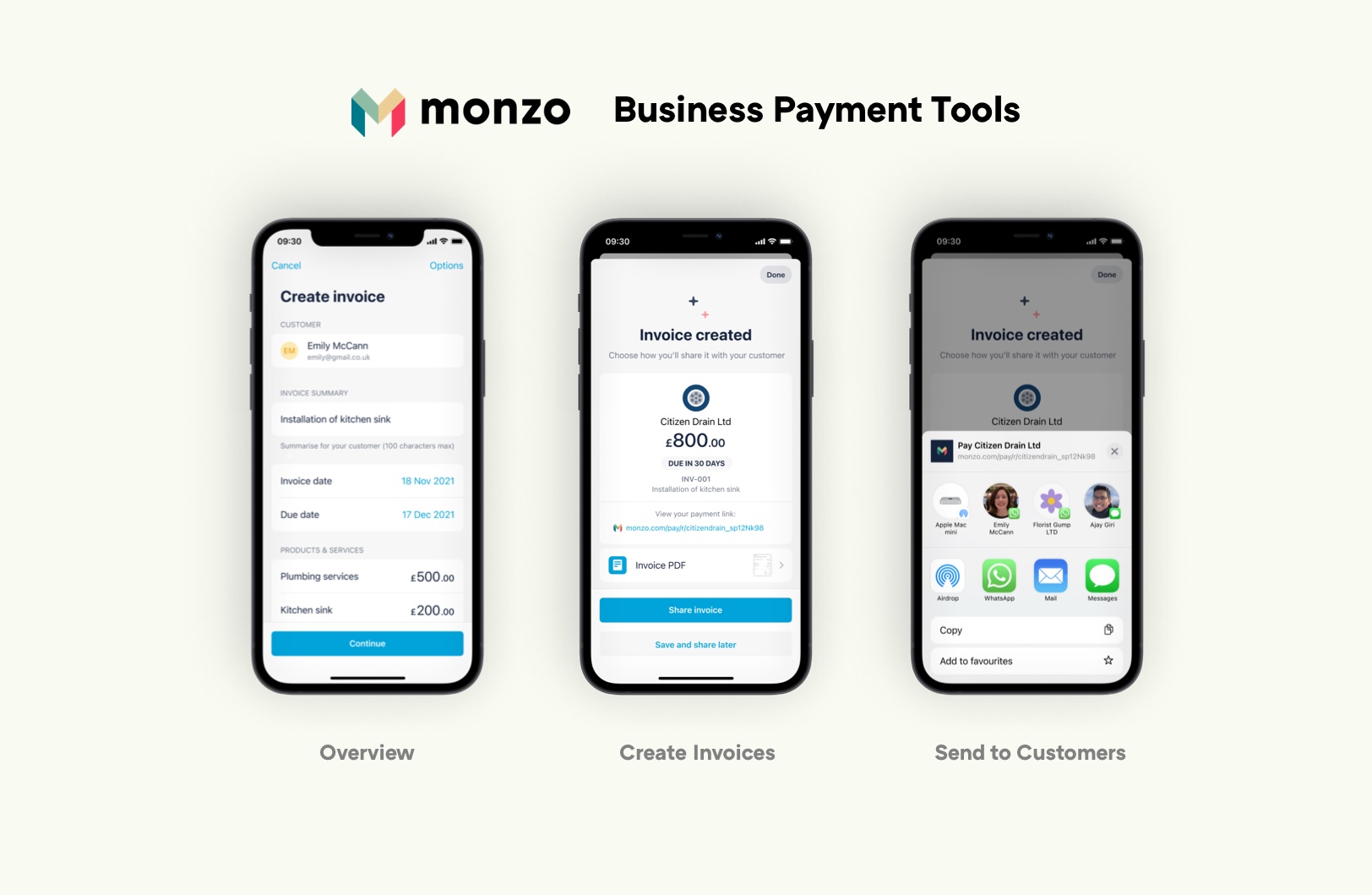

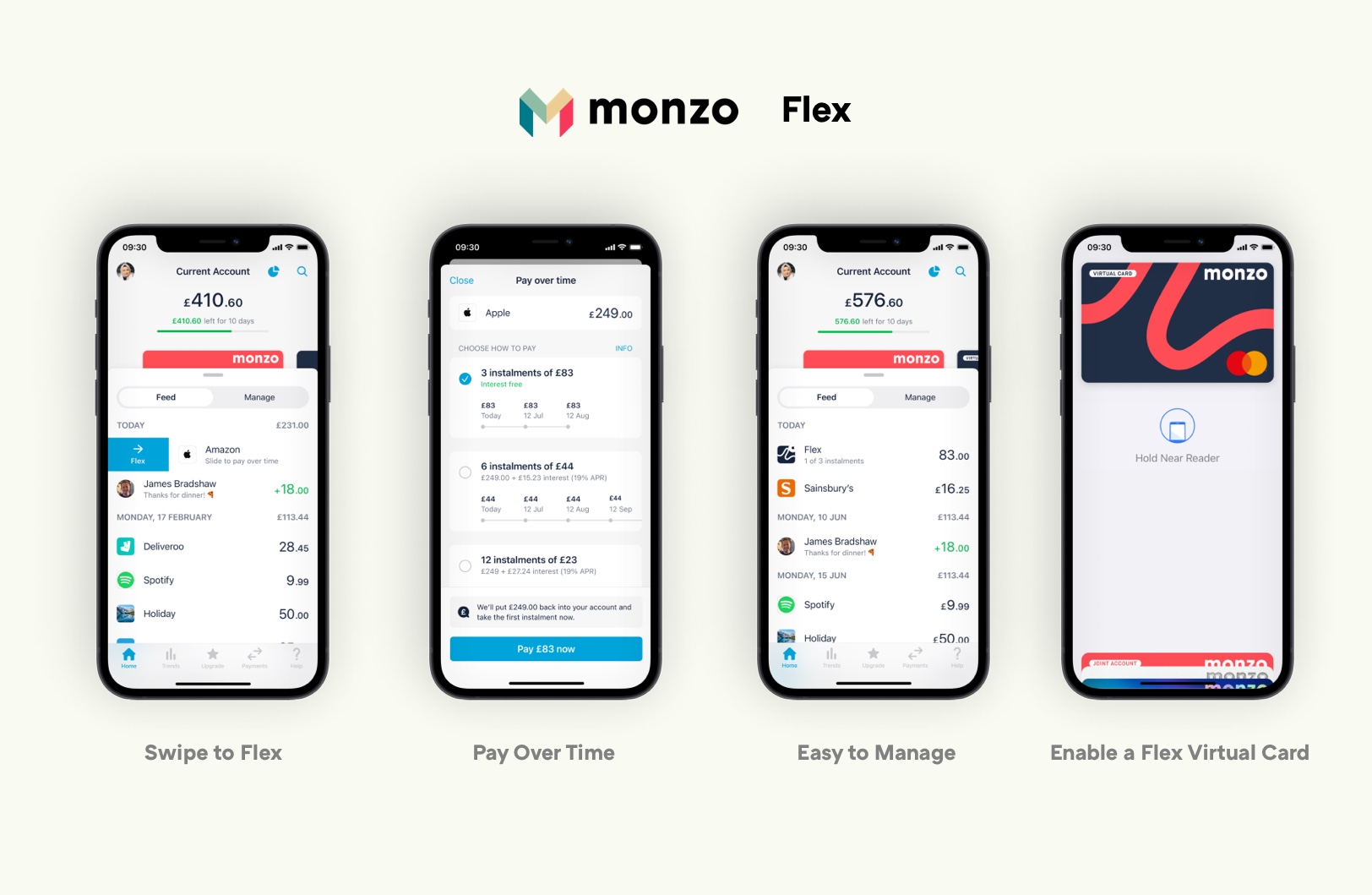

deep dives</a> on the problems and what they did to fix them.</p><p>As Monzo has scaled to become the leading neobank in the UK, it has continued to mindfully launch features with an emphasis on treating customers fairly and having a positive social impact. Our five favorite examples are outlined below:</p><p><strong><strong>(1) Gambling block:</strong></strong> One of the features that best highlights Monzo’s commitment to better money management is <a href=https://www.ycombinator.com/"https://monzo.com/i/gambling-block/">Gambling Block</a>, a feature where customers can disable transactions tagged as gambling. This feature might seem counterintuitive for banks traditionally incentivized to maximize monthly spend and revenue. But Monzo’s employees enthusiastically believed Gambling Block advanced the company’s customer-centric vision by encouraging better spending habits. The feature was actually devised by a small team of Monzonauts during “Monzo Time,” a monthly event during which employees can work on anything important to them. As of February 2021, Gambling Block was being used by 275,000 customers and was blocking nearly 600,000 transactions per month.</p><p><strong><strong>(2) Tone of voice guide:</strong></strong> In 2017, Monzo published a <a href=https://www.ycombinator.com/"https://monzo.com/tone-of-voice//">Tone of Voice</a> guide to maintain its clear, concise, positive voice as it scaled. This includes everything from Monzo’s terms and conditions, which have the required <a href=https://www.ycombinator.com/"https://monzo.com/blog/2018/07/02/the-monzo-mission/">reading age of 11</a>, to the way customer support agents communicate with customers.</p><p><strong><strong>(3) Proactive transparency:</strong></strong> Like all banks, Monzo has visibility into customer spending. Unlike all banks, Monzo uses this visibility to go above and beyond in proactively supporting users. In 2018, Monzo’s financial crime and security team noticed a concentrated number of fraudulent Ticketmaster transactions and immediately updated its systems to block suspicious transactions, alerted relevant parties, and <a href=https://www.ycombinator.com/"https://twitter.com/dan_graf/status/986979971905310720/">proactively replaced</a> customers’ cards. Two months after receiving information from Monzo, <a href=https://www.ycombinator.com/"https://monzo.com/blog/2018/06/28/ticketmaster-breach/">Ticketmaster announced the breach</a> that compromised card details.</p><p><strong><strong>(4) Fair-use fees and customer-friendly lending:</strong></strong> In 2020, Monzo introduced <a href=https://www.ycombinator.com/"https://monzo.com/blog/withdrawal-and-card-delivery-fees/">fair-use fees</a> for customers who used certain features above normal levels and created higher levels of free allowances for customers who used Monzo as their main account. The new fees impacted fewer than 30% of Monzo customers and were well-received by the community. Another example of Monzo’s customer-centric approach is <a href=https://www.ycombinator.com/"https://monzo.com/flex//">Monzo Flex</a>, which is a better way to pay later. Instead of just launching another BNPL product, Monzo asked customers what they liked and disliked about existing lending products. Customers told them they didn’t want to have to reapply every purchase, they wanted flexible payment terms, and they wanted ubiquitous acceptance. Monzo Flex solves these problems by checking for affordability and letting users spread the cost across any purchase with flexible payment terms.</p><p><strong><strong>(5) Internal inclusion goals:</strong></strong> Monzo’s company operating system was also designed with transparency, fairness, and authenticity. The company publishes <a href=https://www.ycombinator.com/"https://monzo.com/blog/our-2020-diversity-and-inclusion-report/">an annual report</a> of its progress on diversity and is on track to reach a <a href=https://www.ycombinator.com/"https://monzo.com/blog/gender-pay-gap-update-april-2020-and-april-2021/">0% gender pay gap</a>. Women make up 40% of their executive team and board. This focus on building an inclusive company operating system is one of the many reasons why Monzo is consistently rated the <a href=https://www.ycombinator.com/"https://www.linkedin.com/pulse/linkedin-top-startups-2021-15-uk-companies-rise-linkedin-news-uk//">number one UK startup</a> on LinkedIn.</p><p>In 2019, Monzo was recognized by <a href=https://www.ycombinator.com/"https://monzo.com/blog/monzo-is-the-uks-most-recommended-brand/">YouGov as not just the most-recommended bank but <u>consumer brand</u>, and in 2020 it was rated the number-one bank for service quality per the <a href=https://www.ycombinator.com/"https://monzo.com/blog/2020/08/17/were-the-best-bank-for-overall-service-quality-and-online-and-mobile-banking/">Competition and Markets Authority</a>. Monzo’s efforts to build a customer centric brand and their focus on building a best-in-class consumer product helped the company scale from 500 to 500,000 users less than 24 months after initial Alpha launch and less than 6 months after launching full bank accounts.</p><h2 id=\"scaling-monzo-growing-to-5m-users-and-100k-businesses-in-5-years\"><strong>Scaling Monzo: Growing to 5M+ users and 100K businesses in 5 years</strong></h2><p>Monzo’s second chapter has been even more impressive. Since launching in the UK five years ago, Monzo has scaled to 5.3 million users, or more than 10% of the adult population. In an incredibly short amount of time, Monzo has managed to turn a good product into a highly competitive platform with a significant market share. And they did it by spending only £20M on marketing in one year, or <£20 per customer. In the years since, they’ve spent £0 on marketing.</p><p><strong><strong>Scaling the customer base efficiently and effectively</strong></strong><br>Monzo used its early enthusiastic community to drive new customer growth. In designing its cards, Monzo chose an eye-catching hot coral color. The card became a conversation piece, as curious bystanders asked Monzo customers about it, which would naturally result in new signups. Monzo then built social features to supercharge word-of-mouth growth. It launched <a href=https://www.ycombinator.com/"https://monzo.com/blog/2016/10/17/wonderful-surprises/">Golden Tickets</a> that customers could give to their friends to skip the waitlist, peer-to-peer payments, and contact list sharing between friends. These social features accelerated user growth to 5% week-over-week and helped Monzo scale to over one million users with effectively zero marketing spend in a sector where customers typically cost <a href=https://www.ycombinator.com/"https://www.which.co.uk/news/2021/08/nationwide-launches-125-switching-bonus-is-it-worth-it//">£100–150 to acquire. Today, the average user has 30 friends on Monzo and 83% of active customers enable P2P payments within their first year. Like “Venmo me” in the US, “Monzo me” has become a fixture in the UK vernacular.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-04-p2p.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><p>Monzo also expanded its product from a spending account to full-fledged bank account and financial control center. In its first few years, Monzo added basic banking features such as overdrafts, cash deposits, and direct debits to reach feature parity with traditional banking. In the past 18 months, Monzo revamped personal loans and launched premium subscription accounts with software features and perks such as third-party spend and savings tracking, virtual cards, custom categories, credit tracking, exclusive merchant discounts, and insurance. Today, Monzo isn’t just a complete bank replacement; it’s the best consumer banking experience in the world.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-05-consumer-banking.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><p>Monzo has successfully scaled its customer support and banking infrastructure alongside its user base. There is an entire product team dedicated to building software for customer support agents to surface customer information in seconds and maintain a consistent customer voice across every interaction. This is an enduring advantage over peers that rely on third-party software or automated support systems.</p><p>Monzo has also scaled its internal banking infrastructure. When it first launched, Monzo partnered with third-party payment processors to get to market quickly. Over time, Monzo migrated to internal systems and now has the lowest downtime in the entire banking industry (incumbents and startups). With these backend improvements, Monzo has been able to grow from a tiny startup to a major banking platform while maintaining a 70 NPS. In 2021, over 40% of active customers were using Monzo as their main account, up more than 10 percentage points from 2020.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-06-account-usage.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><p><strong><strong>A natural transition to business banking</strong></strong><br>As Monzo’s consumer brand scaled, the team saw an opportunity to launch a banking product for small and medium businesses (SMBs) in the UK. The average business has 6x more deposits than the average consumer customer and Monzo already had more than 250,000 customers that owned a small business. Legacy banks were not meeting SMB needs, with the average business using 10 to 15 different financial products because SMB accounts were designed solely as transaction accounts. To solve this, Monzo launched business banking as a spending account with added software features such as invoicing, tax budgets, multi-user access, and accounting integrations. Since their SMB launch in April 2020, Monzo has organically scaled to over 100,000 businesses, outpacing every competitor. It took their closest competitor two years and significant marketing spend to reach the same scale.</p><p>Looking ahead, the company has an opportunity to serve larger businesses as well, by building financial operations tooling such as payables/receivables software and international payment capabilities. At scale, Monzo will be also uniquely positioned to enable seamless interactions between business customers and personal customers, similar to how Square does in the US.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-07-business-banking.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><h2 id=\"monzo%E2%80%99s-opportunity-a-leading-consumer-and-business-finance-platform\"><strong>Monzo’s opportunity: A leading consumer and business finance platform</strong></h2><p>The success of Monzo’s first five years will naturally lead to continued expansion within and outside of the UK. We think these are the most exciting opportunities for Monzo to disrupt the global banking landscape:</p><p><strong><strong>(1) Using great software to drive deep value for customers:</strong></strong> Monzo is able to maintain customer-friendly fee structures and policies simply by cutting significant infrastructure operating costs. Their subscription banking product, which offers virtual cards, third-party account connections, and advanced budgeting features in exchange for a flat fee is fundamentally disruptive to incumbents. Today, Monzo’s long-term retention of premium customers outperforms incumbent financial services and is more inline with best-in-class consumer subscription companies like Calm, Netflix, and Spotify. Incumbents do not have the engineering talent or infrastructure to compete.</p><p><strong><strong>(2) Leveraging its two-sided network to build unique customer experiences:</strong></strong> Because of its single-country focus, Monzo has been able to achieve deep reach among both consumer and SMB banking customers in the UK. The company now serves 10% of UK consumers, has 50%+ of UK neobank market share, and has 100,000 SMB customers. The company is in a unique position to build a consumer-to-business payment network in the UK, and has started to lay the foundation with products to <a href=https://www.ycombinator.com/"https://monzo.com/blog/2021/10/12/getting-paid-with-monzo-business/">help businesses get paid</a> and <a href=https://www.ycombinator.com/"https://monzo.com/flex//">Monzo Flex</a>.</p><p>With Monzo’s business payments product, SMBs can collect payments via credit card and bank transfers, historically a huge pain point. Instead of sending invoices via email, businesses can send a Monzo payment link to customers. Early data shows high repeat usage, with the experience being meaningfully better when both the SMB and customer are Monzo users. As its two-sided network scales, more money will stay entirely within the Monzo ecosystem, resulting in better economics and experiences for both the company and its customers.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-08-business-payment-tools.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><p><a href=https://www.ycombinator.com/"https://monzo.com/flex//">Monzo Flex</a> is another product that benefits both consumers and businesses. Flex lets users finance purchases over £30 across multiple installments. Monzo’s natural visibility into users’ spending and financial health enables it to create a product that is better for consumers than traditional BNPL options. First, Monzo finances any transaction (offline or online) regardless of merchant partnership. Second, Monzo leverages its banking relationship to run affordability checks on users. This means Monzo will not approve Flex purchases for customers likely to end up in an endless cycle of debt. Traditional BNPL players can’t do this because it threatens their business model of prioritizing spend and merchant conversion. Over time, Monzo can even leverage its scale in the UK to sign partnerships with merchants to reduce costs for consumers. Flex could also disrupt the credit card market, as users use their virtual Flex cards instead of credit cards to finance payments. While early, the company has seen incredible demand for Flex only a few months after launch.</p><figure class=\"kg-card kg-image-card\"><img src=https://www.ycombinator.com/"https://blog.ycombinator.com/wp-content/uploads/2021/12/monzo-09-flex.jpg/" class=\"kg-image\" alt loading=\"lazy\"></figure><p><strong><strong>(3) Launching new financial tools:</strong></strong> The UK banking market remains fairly disaggregated. A customer might use Monzo for banking, eToro for crypto, Freetrade for equities, and Atom for a mortgage. Monzo will continue to expand its offerings through both its own products and third-party partnerships (where Monzo acts as the front end or distribution engine). As one example, Monzo launched a savings marketplace for customers to earn additional returns two years ago. This product scaled to ~£1.5B in deposits and ~15% penetration of its customer base during a period of near-0% interest rates, creating value for both customers (by offering them higher returns) and deposit partners (who would otherwise have to pay large acquisition costs). Over time, Monzo will have increased opportunities to create new experiences for users in investing, crypto (e.g., staking, buying/selling), savings, and lending.</p><p><strong><strong>(4) Expanding internationally:</strong></strong> The company has spent the last 12 months laying the foundation for its US launch. Rather than copy-pasting its home features to new geographies, Monzo is taking the same user-first design and community approach that won it the dominant position in the UK market. Monzo is running US-based community events, publishing a <a href=https://www.ycombinator.com/"https://app.productstash.io/monzo-usa-public-roadmap/">public product roadmap</a>, and consistently adding new features. Monzo has already scaled the US product to 6,000 beta users and has 38,000 users on its waitlist. But unlike when it launched in the UK, Monzo now has five years of history and product work to leverage. This has enabled Monzo to launch features much faster in the US. Because of its strong foundation and country-specific product approach, Monzo is positioned to become a global financial platform and a major banking institution in every market it enters.</p><h2 id=\"conclusion-spend-save-and-manage-your-money-in-one-place\"><strong>Conclusion: Spend, save, and manage your money in one place</strong></h2><p>Five years in, Monzo is just starting its second act. Monzo’s first act was to build the UK’s best consumer and SMB banking product. Their second act will be to make money work for truly everyone by scaling to a global audience. Over the next decade, the global market share of financial services will increasingly shift towards financial technology companies. We are already seeing signs of this shift within YC. Companies like Brex, Groww, Jeeves, Parker, and Point are capturing share from incumbents in their respective markets. Monzo will be one of the main beneficiaries of this shift, as it continues to compound its lead in the UK and drive growth in new markets.</p><p><em><em>Thank you to Max Winston, the entire Monzo team, Mia Mabanta, and Chloe Gordon for reading multiple drafts of this essay, and to Zain Ali for designing the graphics.</em></em></p><hr><p><sup><strong>1</strong></sup> Financial Conduct Authority – Strategic Review of Retail Banking Business Models <a href=https://www.ycombinator.com/"https://blog.ycombinator.com/monzo-makes-money-work-for-everyone/#footnoteid1\">↩</a><br><sup><strong>2</strong></sup> YC UK Survey on Consumer Banking – 2018 <a href=https://www.ycombinator.com/"https://blog.ycombinator.com/monzo-makes-money-work-for-everyone/#footnoteid2\">↩</a><br><sup><strong>3</strong></sup> Data from Monzo <a href=https://www.ycombinator.com/"https://blog.ycombinator.com/monzo-makes-money-work-for-everyone/#footnoteid3\">↩</a><br><sup><strong>4</strong></sup> Public Filings and FCA’s Retail Banking Market Investigation <a href=https://www.ycombinator.com/"https://blog.ycombinator.com/monzo-makes-money-work-for-everyone/#footnoteid4\">↩</a></p>","comment_id":"61ba442d495e820001cd7ac6","feature_image":"/blog/content/images/2021/12/monzo-01.jpg","featured":false,"visibility":"public","email_recipient_filter":"none","created_at":"2021-12-15T11:38:21.000-08:00","updated_at":"2022-01-29T19:00:42.000-08:00","published_at":"2021-12-08T11:39:00.000-08:00","custom_excerpt":"Scaling a startup is hard. Scaling a startup bank is even harder. Scaling a consumer-focused financial platform—that is also now the primary bank account for millions of UK consumers—in the midst of a once in a century pandemic is close to impossible.","codeinjection_head":null,"codeinjection_foot":null,"custom_template":null,"canonical_url":null,"authors":[{"id":"61fe29e3c7139e0001a710b2","name":"Nic Dardenne","slug":"nic-dardenne","profile_image":"/blog/content/images/2022/02/Nic.jpg","cover_image":null,"bio":"Nic is a principal at YC Continuity. Nic has helped support the teams at Brex, Convoy, Faire, Groww, Monzo, Rappi, Segment, Snapdocs, and Vouch. Before YC, Nic worked as an analyst at Morgan Stanley.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/nic-dardenne/"},{"id":"61fe29e3c7139e0001a7107b","name":"Anu Hariharan","slug":"anu-hariharan","profile_image":"/blog/content/images/2022/02/Anu.png","cover_image":null,"bio":"Anu is a Managing Director & Partner at YC Continuity. Previously, Anu was a Partner at a16z, where she worked actively with the management teams of companies including Airbnb, Instacart, and Medium.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/anu-hariharan/"}],"tags":[{"id":"61fe29efc7139e0001a7116d","name":"Essay","slug":"essay","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/essay/"},{"id":"61fe29efc7139e0001a71170","name":"Startups","slug":"startups","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/startups/"},{"id":"61fe29efc7139e0001a71182","name":"#ycc","slug":"hash-ycc","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"61fe29efc7139e0001a71181","name":"YC Continuity","slug":"yc-continuity","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/yc-continuity/"},{"id":"61fe29efc7139e0001a711b6","name":"#4787","slug":"hash-4787","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"}],"primary_author":{"id":"61fe29e3c7139e0001a710b2","name":"Nic Dardenne","slug":"nic-dardenne","profile_image":"https://ghost.prod.ycinside.com/content/images/2022/02/Nic.jpg","cover_image":null,"bio":"Nic is a principal at YC Continuity. Nic has helped support the teams at Brex, Convoy, Faire, Groww, Monzo, Rappi, Segment, Snapdocs, and Vouch. Before YC, Nic worked as an analyst at Morgan Stanley.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/nic-dardenne/"},"primary_tag":{"id":"61fe29efc7139e0001a7116d","name":"Essay","slug":"essay","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/essay/"},"url":"https://ghost.prod.ycinside.com/monzo-makes-money-work-for-everyone/","excerpt":"Scaling a startup is hard. Scaling a startup bank is even harder. Scaling a consumer-focused financial platform—that is also now the primary bank account for millions of UK consumers—in the midst of a once in a century pandemic is close to impossible.","reading_time":15,"access":true,"og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"email_subject":null,"frontmatter":null,"feature_image_alt":null,"feature_image_caption":null},"mentions":[{"id":4787,"slug":"monzo-bank","name":"Monzo Bank","batch_name":null,"small_logo_url":"https://bookface-images.s3.amazonaws.com/small_logos/b1262acc9e79773337df0be8c8de0cd79a0a813f.png","one_liner":"A bank as smart as your phone.","website":"http://www.monzo.com","long_description":"YC has written a good overview of our business on their blog: https://blog.ycombinator.com/monzo-makes-money-work-for-everyone/\r\n\r\nOur mission is to make money work for everyone. We are the UK's leading digital bank for individuals and businesses, reinventing the traditional banking industry one customer at a time. We're relentlessly mission driven and always put our customers first - from what products we chose to launch next to our transparency and use of simple language. With a Net Promoter Score of 70+, it shows. \r\n\r\nFrom our founding in 2015, we now have over 7 million customers in the UK (13% of UK adults) and are building out our team in the US. We've seen incredible organic growth, acquiring 150,000 customers / month in 2022, with 80% of this coming from word of mouth. Our weekly active user rate is ~60% and ~40% of our active users use us as their Main Bank account, showing that we are a product that is embedded in our users' daily lives. We've grown to ~2,450 staff (~400 of which make up the product/tech team), and are backed by YC, Stripe, Tencent, Mike Moritz, and others.\r\n\r\nInternally, we encourage an open, collaborative, and inclusive working environment - we were voted the #1 startup where people in the UK want to work for the second year running in 2022. We contribute to open source software, and we continually engage with our wonderful community. We're hiring talented, creative problem-solvers to help us build the bank of the future. Join us!","tags":[],"ycdc_status":"Active","logo_url":"https://bookface-images.s3.amazonaws.com/logos/e6339a9fe79d04ef9171714ff332babf19b659f2.png","year_founded":2015,"team_size":2450,"location":"London, United Kingdom","linkedin_url":"https://www.linkedin.com/company/monzo-bank/?originalSubdomain=uk","twitter_url":"https://twitter.com/monzo","fb_url":"","cb_url":"https://www.crunchbase.com/organization/monzo","is_hiring":true,"active_job_count":0}],"related_posts":[{"id":"63d45276ba7a5900012d1cb7","uuid":"539ff8b7-1511-483b-aade-1dccd48511b1","title":"Learnings of a CEO: Snapdocs’ Aaron King on navigating market cycles","slug":"learnings-of-a-snapdocs-aaron-king-on-navigating-market-cycles","html":"<p>Welcome to the fourth edition of Learnings of a CEO. You can read previous editions <a href=https://www.ycombinator.com/"https://www.ycombinator.com/blog?query=learnings%20of%20a%20CEO\%22>here. </p><p><a href=https://www.ycombinator.com/"https://www.snapdocs.com//">Snapdocs is the leading digital closing platform for the mortgage industry. Today, the company touches 25% of all US real estate transactions and is valued at $1.5B. Founder and CEO <a href=https://www.ycombinator.com/"https://twitter.com/a_w_king/">Aaron King</a> and his team have expertly navigated fundraising and market cycles. We sat down with Aaron to hear his insight into getting a business up and running with minimal outside funding and building through volatile market conditions. </p><p><strong>Why did you decide to raise minimal funding early in the company’s history?</strong></p><p>I never considered funding to be a requirement for building — but I also didn't know much about fundraising early on in the company’s history. Snapdocs was started as a side project a couple of years before ever thinking about applying to YC. By the time I applied, we had a live product, customers, and revenue. Even after YC, we didn’t raise much immediately. We stayed focused on building and then raised a seed round later in the year.</p><p>It wasn’t until three years later that we raised our Series A. By then, we had spent about $1MM of our seed round and were at a $5MM revenue run rate. Around that time we started working with much larger customers, and it was clear we would need more capital to be successful in this bigger market. So, we raised our Series A. After we closed the round, our lead investor revealed how capital efficient we had been compared to our peers. </p><p><strong>Do you feel you had to ruthlessly prioritize when building the product because you didn't have the capital?</strong></p><p>Yes, and I’ve learned that you should take the same approach even when you do have the capital to be less disciplined. Back then, ruthless prioritization was our only option. We couldn’t afford to build features that weren’t essential. There were always a hundred distractions that would result in a broader, less focused product. But our capital constraints kept us focused on going deep with our paying customers. That helped us avoid the common trap of building products no one wanted. </p><p>It also meant that when we decided to build a product, we had to think about the smallest version of that product in order to quickly ship. That helped ensure we had a short feedback loop from our users and ensure our resources were continuously being invested in building the right features. Looking back, I’m amazed at how much we were able to accomplish without spending much capital. </p><p>Being capital constrained forced good behaviors that served us well even after we raised more funding. We continue to be thoughtful about every dollar we spend. But, there is a cost to this approach, and we’re paying for it today. We built many things that weren't engineered for scale or flexibility. However, now we can afford to reengineer those unscalable solutions because we built something people want.</p><p><strong>What did your product cycles look like before you raised your Series A?</strong></p><p>We were always heavy on customer involvement when building product. We spent a lot of time in our customers’ offices watching them use what we were building and understanding their work. We also kept a lot of our prospects in the loop as we built new features. Some of the best feedback came from people who had chosen to not yet work with us. Responding to that feedback with a killer feature was a great way to ultimately get them on board. </p><p>We built a lot of trust and rapport with these early customers, and the in-person interactions helped immensely. As a result, they would call one of us the moment they thought there was a problem or if they thought a competitor was doing something compelling. Customer churn for Snapdocs has always been incredibly low as a result. </p><p>We created a disciplined product release process, even in those early days, but we were still able to move quickly. We shipped code every day, sometimes multiple times a day. Customers were impressed by how quickly we could respond to issues and feedback. </p><p>Interestingly, not having too much pressure from investors early on allowed us to experiment more in an underappreciated part of our market. The Serviceable Available Market (SAM) of our initial product was roughly only $20MM, but we believed it would allow us to expand into more critical parts of the mortgage ecosystem. It was the type of opportunity that would be hard to discover through market analysis or spreadsheet exercises. You had to get deep into the problem set to see the opportunity and develop the right strategy—and that ultimately worked to our advantage. </p><p><strong>Founders need capital to hire employees. As a bootstrapped company, what was your strategy around hiring? </strong></p><p>Hiring was hard, but we did a few things that worked well. Even before the company could afford full-time employees, I worked with talented contractors. I also leaned on friends to help me work through both technical and business challenges. Someone would come over and whiteboard with me or we’d get into the code and work through a problem. </p><p>When I could afford to hire full-time employees, I treated them like founding team members. I was generous with equity and shared everything about the potential and challenges of the business. We built a lot of trust as a small team. Getting a few really good people into the company early on was foundational to the company’s success. </p><p>The first person to join full-time was an engineer I had worked with in a previous role (and one of the friends that would help in those early days). The second and third hires were applicants from job postings on Hacker News. All three turned out to be excellent. None of us initially had large networks in the startup world, so most of our early hiring involved lots of interviews and hiring a few of the wrong people. We couldn’t attract well-known talent and took risks; invested in people we thought had a lot of potential. </p><p>One mistake I made in the early years was being too timid to approach more of the people I respected. I should have tried to convince them to quit their successful jobs and join our small (yet risky at the time) startup. I’m fearless on this approach now, but back then I was intimidated to try to convince a friend to join a company that might fail. In hindsight, I did them a disservice by not trying to recruit them. The truth is that these people are smart and you’re not harming anyone by sharing your vision and the potential of the company with them. As long as you’re honest and transparent about the inherent challenges, you should give them the opportunity to take a risk on you. </p><p>As Snapdocs grew, it became easier to pull from the team’s networks. We continued to build a lot of trust within the team, and they started referring their friends to apply. Eventually, we attracted well-known investors, and that, along with our culture and growth, made hiring easier. </p><p>Because we were capital constrained, we also didn’t hire anyone until there was a clear and painful need. It made running the company harder because we were all spread thin but ultimately made us incredibly productive, as it meant we were always working on the most important things. </p><p><strong>How have you navigated different market conditions? When do you decide to react?</strong></p><p>A big part of our success has come from selectively ignoring some market changes while reacting quickly to others. It has always been a question of how the change aligns with our resources, vision, and north star metric of market share growth. </p><p>For example, the biggest and most dynamic change we regularly experience are fluctuations in the number of mortgages that happen in a given month or year. This can change quickly based on a host of economic factors. When we are well-resourced and growing fast, we can ignore some of those market downturns and stay focused on market share growth — knowing we have the momentum and capital to power through it. Other times we’ve had to scale up or scale back based on the size of the fluctuation.</p><p>But other market dynamics can change quickly too, like the industry’s appetite for new technologies and the competitive landscape. There have been times when the market was demanding a technology but we believed there were underlying factors in the industry that would prevent that tech from scaling. If we built the technology, it would pull resources away from the priorities that drove us toward our long-term goals. And so, sometimes to the protests of our sales team, we ignored it or invested minimally in these trendy areas. By doing so, we were able to stay focused on the things that were truly going to transform the industry. </p><p>It’s also worth noting that navigating change was relatively easy in the first few years of building the company. It was a lot easier to adjust course on company direction or strategy when the team was smaller and could all fit in the same room. The product cycles were relatively short and malleable. The cost of making a change was low. </p><p>As the company has grown, we’ve had to be a lot more thoughtful and methodical about changing the speed or direction of the business as we react to market changes. The cost of making a change has increased a lot. Investments take longer to play out. Changes to headcount take longer to scale up or down. There are more people on the team and more layers in the organization to communicate the change through. </p><p><strong>In March 2020, Snapdocs made a huge shift because of changes you were seeing in the housing market. How did you communicate this shift to your team and ensure their goals were aligned with the new priorities? </strong></p><p>COVID accelerated demand for our product, but with that came a shift in what our customers wanted from a platform like ours. We had to expand quickly to serve their needs, and we had to pivot our roadmap on a dime. It’s a testament to the team that we were able to pull that off. </p><p>To make decisions quickly and then communicate them, we worked in concentric circles. We started by discussing the change in a smaller group of 3-4 people. This is where the hardest and messiest conversations took place. We moved quickly to define the problems and opportunities and set a direction for the company. We then looped in the senior leadership team for further discussion and to arm them with everything they needed to share the directional changes with their teams. Finally, we held a company-wide meeting to share the new direction and answer questions. All of this happened over the course of about 2 weeks.</p><p>Now, our business required more speed and flexibility as information was coming in and changing week on week. We dealt with this by creating temporary pods of 4-5 team members focused on solving specific challenges that would spin up for a few weeks and then dissolve once the challenge was addressed. We also increased the frequency of our company-wide all-hands meetings from monthly to weekly so we could keep the whole company up to speed. </p><p>Luckily we had a deep culture of transparency that goes back to the beginning of the company. We’ve always tried to share everything with our entire team — our cash balance, monthly growth rate, burn, our biggest challenges. This got harder as the team grew, but we’ve largely continued this transparency to today. It’s much easier to be transparent in times of great change if you've laid a foundation of trust and transparency in the past. </p><p>We also worked hard to be intellectually honest about the growth we were experiencing. It’s easy to take credit when the business accelerates, but our message to the team wasn't, “Look at how great we're doing.” The message was closer to, “This industry works in cycles. We're in an up cycle now and that's great. There's going to be a down cycle. We don't know when or how strong it's going to be. But we should not overly congratulate ourselves for the current situation, just as we shouldn’t be too hard on ourselves when we’re fighting through an inevitable downturn in the future.”</p><p><strong>In 2021, Snapdocs </strong><a href=https://www.ycombinator.com/"https://www.snapdocs.com/resource-center/blog/announcing-our-150m-series-d-funding-round/">announced a Series D round. How did this change your mentality around resources?</strong></p><p>It was clear that the pandemic would be an accelerator for our business, and we needed to move fast to stay ahead of the market. We went from being frugal to raising larger rounds of capital and hiring seasoned executives who could help us scale. It’s important for companies to evolve at the right points in time and ask themselves, “Is what I did yesterday the thing that's going to get me to where I need to be tomorrow?”. We asked that question and decided we needed to change parts of our culture and capital investment strategy if we wanted to win.</p><p>When we raised capital in 2021, transactions on Snapdocs had steadily increased to millions of closings a year and thousands of lenders and title companies were using our technology every month. Demand for mortgages throughout the pandemic was strong, and we deployed an intentional strategy of prioritizing effectiveness over efficiency. We needed to get aggressive and expand our market position, which required capital. </p><p>The market turned again later in the year, with demand for mortgages cooling. It was clear that it was time to go back to some of our old ways of doing things. We ditched the motto of being effective over being efficient. This meant a return to ruthless prioritization of our focus. We shifted away from investing so heavily in future scale as we wouldn’t need to tap into these systems for a few years.</p><p>I find it helpful to remember that market fluctuations are normal and unavoidable. Startups should scale up at times and scale back at others. It’s hard and painful. There’s nothing easy or enjoyable about being understaffed to meet customer demand on one side, or needing to let team members go on the other. But these ups and downs are natural and a necessary part of building an enduring company. In a startup, you’re always making hard decisions based on insufficient information. You’re never going to be able to perfectly predict the future. You need to keep making the best decisions you can — knowing all the while that you may be wrong and need to change course again once the future becomes clearer.</p>","comment_id":"63d45276ba7a5900012d1cb7","feature_image":"/blog/content/images/2023/02/BlogTwitter-Image-Template--24-.png","featured":true,"visibility":"public","email_recipient_filter":"none","created_at":"2023-01-27T14:38:46.000-08:00","updated_at":"2023-02-22T18:17:22.000-08:00","published_at":"2023-01-30T08:59:00.000-08:00","custom_excerpt":"Founder & CEO Aaron King expertly built Snapdocs through volatile market conditions and with minimal outside funding into the mortgage industry's leading digital closing platform, valued at $1.5B today. This is what he learned about navigating market cycles.","codeinjection_head":null,"codeinjection_foot":null,"custom_template":null,"canonical_url":null,"authors":[{"id":"61fe29e3c7139e0001a710a7","name":"Lindsay Amos","slug":"lindsay-amos","profile_image":"/blog/content/images/2022/02/Lindsay.jpg","cover_image":null,"bio":"Lindsay Amos is the Senior Director of Communications at Y Combinator. In 2010, she was one of the first 30 employees at Square and the company’s first comms hire.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/lindsay-amos/"}],"tags":[{"id":"61fe29efc7139e0001a71174","name":"Advice","slug":"advice","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/advice/"},{"id":"61fe29efc7139e0001a71181","name":"YC Continuity","slug":"yc-continuity","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/yc-continuity/"},{"id":"61fe29efc7139e0001a71152","name":"Founder Stories","slug":"founder-stories","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/founder-stories/"},{"id":"61fe29efc7139e0001a71158","name":"Leadership","slug":"leadership","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/leadership/"},{"id":"61fe29efc7139e0001a71170","name":"Startups","slug":"startups","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/startups/"},{"id":"61fe29efc7139e0001a71155","name":"Growth","slug":"growth","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/growth/"},{"id":"63d45389ba7a5900012d1ccf","name":"#622","slug":"hash-622","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"}],"primary_author":{"id":"61fe29e3c7139e0001a710a7","name":"Lindsay Amos","slug":"lindsay-amos","profile_image":"https://ghost.prod.ycinside.com/content/images/2022/02/Lindsay.jpg","cover_image":null,"bio":"Lindsay Amos is the Senior Director of Communications at Y Combinator. In 2010, she was one of the first 30 employees at Square and the company’s first comms hire.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/lindsay-amos/"},"primary_tag":{"id":"61fe29efc7139e0001a71174","name":"Advice","slug":"advice","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/advice/"},"url":"https://ghost.prod.ycinside.com/learnings-of-a-snapdocs-aaron-king-on-navigating-market-cycles/","excerpt":"Founder & CEO Aaron King expertly built Snapdocs through volatile market conditions and with minimal outside funding into the mortgage industry's leading digital closing platform, valued at $1.5B today. This is what he learned about navigating market cycles.","reading_time":9,"access":true,"og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"email_subject":null,"frontmatter":null,"feature_image_alt":null,"feature_image_caption":null},{"id":"63f91878d2b0220001e8d6e9","uuid":"a99f2458-1bdd-4a40-81e6-36ee441b133c","title":"Congratulations to the 2023 YC Top Companies!","slug":"yc-top-companies-feb-2023","html":"<p>We’re excited to present the 2023 YC Top Companies!</p><p>The startups are separated into 3 lists: YC’s top <a href=https://www.ycombinator.com/"https://www.ycombinator.com/topcompanies/" rel=\"noopener noreferrer\">private</a>, <a href=https://www.ycombinator.com/"https://www.ycombinator.com/topcompanies/public/" rel=\"noopener noreferrer\">public</a>, and <a href=https://www.ycombinator.com/"https://www.ycombinator.com/topcompanies/exits/" rel=\"noopener noreferrer\">exited</a>. Private companies and exits are sorted by the company's valuation from their latest funding round, and all are valued at over $150M. Public companies are listed in alphabetical order.</p><p>The Breakthrough Companies list highlights the fast-growing companies we’ve doubled down on – which means they’ve all received significant additional investment from YC in their post-Demo Day rounds. </p><p><strong>Here are stats about the companies on this year’s list:</strong></p><p><strong>></strong> More than 290 private YC companies and 33 exits are valued at over $150M, over 90 are worth more than $1B, and 16 are public. </p><p><strong>></strong> 58% of the companies have HQs in the Bay Area. 27% of the companies are fully remote, and 55% list themselves as partially remote.</p><p><strong>></strong> YC Top Companies have HQs in 40 countries including: United States, India, United Kingdom, Canada, Colombia, Indonesia, Mexico, Nigeria, Argentina, Brazil, Chile, France, Spain, Israel, Netherlands, Philippines, Portugal, Germany, Egypt, Ireland, South Korea, Peru, Singapore, United Arab Emirates, Australia, Bolivia, Switzerland, Algeria, Estonia, Finland, Hungary, Italy, Norway, Romania, Sweden, Senegal, Uganda, Uruguay, Venezuela, Vietnam</p><p><strong>></strong> YC W16 is the most represented batch (by percentage). 23% of the companies from W16 are on the YC Top Companies list. </p><p><strong>></strong> Here’s a sector breakdown of the top companies:</p><ul><li>B2B Software and Services: 43%</li><li>Financial Technology and Services: 19%</li><li>Consumer: 13%</li><li>Healthcare: 12%</li><li>Industrials: 7%</li><li>Real Estate and Construction: 3%</li><li>Education and Government: 3%</li></ul><p><strong>></strong> 10 new companies joined the lists since August 2022:</p><p>Private:</p><ul><li><a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/treasury-prime/">Treasury Prime</a> (YC W18) - Embedded banking software platform and marketplace</li><li><a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/onesignal/">OneSignal (YC S11) - Engage customers through personalized omni-channel messaging</li><li><a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/skill-lync/">Skill-lync (YC W19) - Online engineering college for India</li><li><a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/tigereye/">TigerEye (YC S22) - Modern enterprise software for sales leaders</li><li><a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/zeitview/">Zeitview (YC W15) - Inspection software for renewable energy & sustainable infrastructure</li><li><a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/ontop/">OnTop (YC W21) - A bank for remote workers connected to payroll</li><li><a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/obie/">Obie (YC S19) - Insurance and risk management for landlords</li><li><a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/nabis/">Nabis (YC W19) - The largest licensed cannabis wholesale platform</li></ul><p>Public:</p><ul><li><a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/presto/">Presto (YC S10) - Digital meets physical for big chain restaurants</li></ul><p>Exits:</p><ul><li><a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/nurx/">NURX (YC W16) - Medicine or testing kit, prescribed online, and delivered to your door </li></ul><p>One thing to note is that this is not an exhaustive list of YC’s top companies. We allowed founders to opt out of being listed for any reason. The full list of YC companies can be found <a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/">here. </p><p>Congrats again to the companies recognized on the 2023 YC Top Companies list!</p>","comment_id":"63f91878d2b0220001e8d6e9","feature_image":"/blog/content/images/2023/02/BlogTwitter-Image-Template.png","featured":true,"visibility":"public","email_recipient_filter":"none","created_at":"2023-02-24T12:05:12.000-08:00","updated_at":"2023-03-16T09:44:58.000-07:00","published_at":"2023-02-27T09:00:00.000-08:00","custom_excerpt":"There are now 16 public YC companies, 290 private YC companies and 33 exits that are valued at over $150M, and over 80 that are worth more than $1B.","codeinjection_head":null,"codeinjection_foot":null,"custom_template":null,"canonical_url":null,"authors":[{"id":"61fe29e3c7139e0001a7106f","name":"Y Combinator","slug":"yc","profile_image":"/blog/content/images/2022/02/yc.png","cover_image":null,"bio":null,"website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/yc/"}],"tags":[{"id":"61fe29efc7139e0001a71173","name":"YC News","slug":"yc-news","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/yc-news/"},{"id":"61fe29efc7139e0001a71170","name":"Startups","slug":"startups","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/startups/"},{"id":"61fe29efc7139e0001a71181","name":"YC Continuity","slug":"yc-continuity","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/yc-continuity/"},{"id":"63f91d15d2b0220001e8d70c","name":"#177","slug":"hash-177","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"63f91d15d2b0220001e8d70d","name":"#1810","slug":"hash-1810","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"62ba0d42063d2d0001f0fc7a","name":"#76","slug":"hash-76","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"63f91d15d2b0220001e8d70e","name":"#12234","slug":"hash-12234","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"63d1aa7a466acf0001099b6a","name":"#25267","slug":"hash-25267","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"63f91d15d2b0220001e8d70f","name":"#762","slug":"hash-762","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"63f91d15d2b0220001e8d710","name":"#23238","slug":"hash-23238","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"63f91d15d2b0220001e8d711","name":"#12600","slug":"hash-12600","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"63f91d15d2b0220001e8d712","name":"#11995","slug":"hash-11995","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"}],"primary_author":{"id":"61fe29e3c7139e0001a7106f","name":"Y Combinator","slug":"yc","profile_image":"https://ghost.prod.ycinside.com/content/images/2022/02/yc.png","cover_image":null,"bio":null,"website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/yc/"},"primary_tag":{"id":"61fe29efc7139e0001a71173","name":"YC News","slug":"yc-news","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/yc-news/"},"url":"https://ghost.prod.ycinside.com/yc-top-companies-feb-2023/","excerpt":"There are now 16 public YC companies, 290 private YC companies and 33 exits that are valued at over $150M, and over 80 that are worth more than $1B.","reading_time":2,"access":true,"og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"email_subject":null,"frontmatter":null,"feature_image_alt":null,"feature_image_caption":null},{"id":"6356a9c957e9f90001984b62","uuid":"32e1602f-ec89-49b0-932c-61ef6bbacfcb","title":"YC Founder Firesides: Mutiny on AI and the next era of company growth","slug":"yc-founder-firesides-mutiny-on-ai-and-the-next-era-of-company-growth","html":"<p><a href=https://www.ycombinator.com/"https://www.mutinyhq.com//">Mutiny (<a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/mutiny/">YC S18</a>) uses AI and data to convert website visitors into customers. Today, the fastest growing B2B companies such as Notion and Snowflake use Mutiny to identify ideal customers, determine sections of websites that will increase conversion, and produce copy that converts visitors into customers. </p><p>YC’s <a href=https://www.ycombinator.com/"https://twitter.com/anuhariharan/status/1557784730543632384/">Anu Hariharan</a> sat down with Mutiny co-founder and CEO <a href=https://www.ycombinator.com/"https://twitter.com/jalehr/">Jaleh Rezaei</a> to talk about their <a href=https://www.ycombinator.com/"https://twitter.com/jalehr/status/1582352047659024385/">recent acquisition</a> of Intellipse, an AI marketing platform, as well as how AI will impact the next era of growth. Throughout, Jaleh shares advice about acquisitions as a growth strategy and evolving your product with AI. </p><p>You can listen here or on <a href=https://www.ycombinator.com/"https://open.spotify.com/episode/7dy1qB7XQfOryE4kj4spGS/">Spotify, <a href=https://www.ycombinator.com/"https://podcasts.apple.com/us/podcast/160-yc-founder-firesides-mutiny-on-ai-and-the-next/id1236907421?i=1000583708925\%22>Apple Podcasts</a>, and <a href=https://www.ycombinator.com/"https://twitter.com/i/spaces/1yNxaNzAPPnKj/">Twitter.

Notion drives 60% more leads through paid marketing</a></li><li>Example 2: <a href=https://www.ycombinator.com/"https://www.mutinyhq.com/blog/the-second-lever-replays#conversion-secret-how-snowflake-runs-abm-at-scale\">Snowflake builds an ABM and enterprise marketing program</a></li></ul><p><strong>12:50</strong> - You recently shared that with data and AI, Mutiny transforms conversion from a niche A/B testing tool to a platform that every go-to-market team can use to drive efficient growth at scale. What does that mean, and how have you leveraged the advances in AI over the last four years? </p><ul><li>When you can give the entire go-to-market team x-ray vision into every visitor and how they are converting – and then pair that insight with the ability to change the website for different segments – every team will make the website a core part of their strategy to drive more revenue. Mutiny uses AI to give teams this insight and answer questions like: What segments should I prioritize? What parts of the website should I change? What copy will resonate? Where should I focus? </li></ul><p><strong>17:00</strong> - At Mutiny when looking at data, when do you know the right questions to ask and when do you say these are not questions we need to optimize now?</p><ul><li>In the early days, one of the most valuable things we did was follow our customers’ growth teams. We would attend team meetings, watch them use our product, and ask questions. It became clear what we should build for our customers. </li></ul><p><strong>20:30</strong> - Since you started Mutiny, what are some of the advances in AI that you’ve leveraged? </p><ul><li>We did things that didn't scale in the early days to solve customers’ problems. As our customers grew, our data set grew and we used AI models and inputs to improve our recommendation engines and service a broader customer base. Today, we can build models that tell a user where on the website they should make changes and write personalized copy leveraging GPT-3. </li></ul><p><strong>29:10</strong> - Did you have moments when you felt Mutiny could be doing more with the advances being made in AI? </p><ul><li>We saw an opportunity to marry our proprietary data set with GPT-3 to produce highly personalized copy. </li></ul><p><strong>32:15</strong> - GPT-3 was an inflection point for Munity. What is the next inflection point? </p><ul><li>There are a lot of opportunities with DALL-E, as visuals are important in marketing.</li></ul><p><strong>36:30</strong> - Do you have cautionary advice on how to think about using technologies like GPT-3 and DALL-E for founders dabbling in AI? </p><ul><li>Think through the ultimate long-term vision of the product and the long-term defensibility of the business. And launch fast, as technology develops quickly. </li></ul><p><strong>38:40</strong> - What advice do you have for founders in terms of leveraging OpenAI, GPT-3, etc. while focusing on the long-term vision? </p><ul><li>Your vision and long-term view is separate from your day-to-day execution. Your long-term vision (i.e. the opportunity and what you’re trying to create over the course of a decade) provides clarity around where you’re trying to go and brings other people along with you, like your investors and employees. Day-to-day, you’re focused and executing quickly – and not always thinking about the ten year vision when you’re building V1.</li></ul><p><strong>43:45</strong> - You decided to grow your team by acquiring Intellipse. And now, Mutiny has one of the larger engineering teams with production experience in modern marketing AI technologies. Why did you decide to pursue an acquisition? </p><ul><li>Founders have to look for inflection points where something happens in the market leading to the “old way” no longer being as good. And as a result, a much larger portion of the market is open to a new and better way. We’re in a recession, and this is an inflection point for Mutiny. Companies need to convert every dollar to a customer, and Mutiny has built a product that makes marketing dollars more efficient. We can accelerate our road map with the acquisition of Intellipse</li></ul><p><strong>46:40</strong> - How did you know you wanted to work with the Intellipse team so much that you had to go through an acquisition?</p><ul><li>We were interested in the Intellipse team and the skills the team had developed. Their CTO and senior engineers had a unique experience with marketing AI and newer technologies, like GPT-3.</li><li>The personality and values of the founder spreads in an organization and becomes the company culture. After getting to know the founder and the free am, it was evident the two companies had a similar culture and shared values – and we’d be able to bring this team in and enhance our culture.</li></ul><p><strong>50:15</strong> - How long did it take to assess the culture? </p><ul><li>We spent the same amount of time with each individual as if we were hiring them onto the team through our typical recruiting process.</li></ul><p><strong>51:30</strong> - Do you expect to acquire more companies in the future? And how should founders and CEOs determine whether this strategy is right for their company? </p><ul><li>Be clear about your goals and why an acquisition is the right way to achieve those goals. When a company is working toward a similar goal – building something we would have done ourselves – it is a successful acquisition. With Intellipse, the team shared similar goals and company culture, and could accelerate our timing.</li><li>We want to hire founders onto our product team who are user focused and move quickly. Founders can focus their entrepreneurial energy on building a product and growing that business area within Mutiny. </li></ul><p><strong>54:55</strong> - What are your thoughts about how AI will impact the next ten years? </p><ul><li>There has been enough productization of backend AI technologies that as a founder you can tap into AI to accelerate the product you want to build and the value you give to customers. From a user and growth perspective, AI enables us to automate many of the tasks no one wants to do. And for those who aren’t technical – but understand what they are trying to do – they can now be self sufficient.</li></ul>","comment_id":"6356a9c957e9f90001984b62","feature_image":"/blog/content/images/2022/10/BlogTwitter-Image-Template-1.jpeg","featured":true,"visibility":"public","email_recipient_filter":"none","created_at":"2022-10-24T08:05:45.000-07:00","updated_at":"2022-10-25T08:44:16.000-07:00","published_at":"2022-10-24T09:25:31.000-07:00","custom_excerpt":"YC’s Anu Hariharan sat down with Mutiny co-founder and CEO Jaleh Rezaei to talk about their recent acquisition of Intellipse, an AI marketing platform, as well as how AI will impact the next era of growth.","codeinjection_head":null,"codeinjection_foot":null,"custom_template":null,"canonical_url":null,"authors":[{"id":"61fe29e3c7139e0001a7106f","name":"Y Combinator","slug":"yc","profile_image":"/blog/content/images/2022/02/yc.png","cover_image":null,"bio":null,"website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/yc/"}],"tags":[{"id":"61fe29efc7139e0001a71170","name":"Startups","slug":"startups","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/startups/"},{"id":"61fe29efc7139e0001a71175","name":"Interview","slug":"interview","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/interview/"},{"id":"61fe29efc7139e0001a71181","name":"YC Continuity","slug":"yc-continuity","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/yc-continuity/"},{"id":"61fe29efc7139e0001a71152","name":"Founder Stories","slug":"founder-stories","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/founder-stories/"},{"id":"61fe29efc7139e0001a71176","name":"Podcast","slug":"podcast","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/podcast/"},{"id":"6312238da32f070001d502c0","name":"#2014","slug":"hash-2014","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"61fe29efc7139e0001a71155","name":"Growth","slug":"growth","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/growth/"},{"id":"61fe29efc7139e0001a71158","name":"Leadership","slug":"leadership","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/leadership/"}],"primary_author":{"id":"61fe29e3c7139e0001a7106f","name":"Y Combinator","slug":"yc","profile_image":"https://ghost.prod.ycinside.com/content/images/2022/02/yc.png","cover_image":null,"bio":null,"website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/yc/"},"primary_tag":{"id":"61fe29efc7139e0001a71170","name":"Startups","slug":"startups","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/startups/"},"url":"https://ghost.prod.ycinside.com/yc-founder-firesides-mutiny-on-ai-and-the-next-era-of-company-growth/","excerpt":"YC’s Anu Hariharan sat down with Mutiny co-founder and CEO Jaleh Rezaei to talk about their recent acquisition of Intellipse, an AI marketing platform, as well as how AI will impact the next era of growth.","reading_time":5,"access":true,"og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"email_subject":null,"frontmatter":null,"feature_image_alt":null,"feature_image_caption":null}]},"url":"/blog/monzo-makes-money-work-for-everyone","version":null,"rails_context":{"railsEnv":"production","inMailer":false,"i18nLocale":"en","i18nDefaultLocale":"en","href":"https://www.ycombinator.com/blog/monzo-makes-money-work-for-everyone","location":"/blog/monzo-makes-money-work-for-everyone","scheme":"https","host":"www.ycombinator.com","port":null,"pathname":"/blog/monzo-makes-money-work-for-everyone","search":null,"httpAcceptLanguage":"en, *","applyBatchLong":"Winter 2024","applyBatchShort":"W2024","applyDeadlineShort":"October 13","ycdcRetroMode":true,"currentUser":null,"serverSide":true},"id":"ycdc_new/pages/BlogPage-react-component-10fecb0a-7c1f-497b-a0ae-d46dcf6d07ce","server_side":true}" data-reactroot="">

Scaling a startup is hard. Scaling a startup bank is even harder. Scaling a consumer-focused financial platform—that is also now the primary bank account for millions of UK consumers—in the midst of a once in a century pandemic is close to impossible.

In April 2020, British banking startup Monzo’s revenue fell by almost 50%. But the company will end 2021 with revenues close to 2x its pre-pandemic peak, in spite of continued low interest rates, reduced travel, and depressed pandemic spending.

This did not happen by magic. Monzo’s culture of customer obsession allowed it to use the crisis to thoughtfully build a beloved consumer and SMB product that has changed personal finance in the UK. In 2022 and beyond, Monzo’s revenues are likely to further accelerate as they benefit from cross border-travel, increased EU interchange rates, and new products.

Banking is a ubiquitous but hard to crack industry. In the United Kingdom alone, there are 73 million personal accounts and four million business accounts, through which customers make more than 40 billion payments per year and hold £1.5 trillion in deposits. Over 96% of UK adults already have a bank account. When Monzo launched in 2015, the big six banks in the UK had more than 85% market share.1

But ubiquity and lack of switching doesn’t necessarily mean customer happiness. In fact, the net promoter score (NPS, a measurement of customer loyalty) of banking in the UK is a very low 18.2 Incumbent banks miss the mark in two crucial areas:

The banking experience has not evolved to match modern consumer expectations. Banks still rely on physical branches and don’t give users the ease of use, feedback, and visibility consumers have come to expect.

Bank business models are not aligned with customer interests. Banks do not incentivize better money habits. Their profit models rely on upselling and non-transparent fees that typically penalize the most vulnerable customers. The average personal account in the UK has £150 to £220 in fees per year, many of which are hidden.

In 2015, Monzo founders Tom Blomfield, Jonas Templestein, Gary Dolman, Jason Bates, and Paul Rippon launched a digital finance platform with the slogan “Make Money Work For Everyone.” The first iteration of the Monzo account was a simple prepaid card that allowed UK customers to open an account online and for free, receive real-time spending notifications, and budget their finances.

Today, Monzo is a full-fledged financial platform that offers customers:

A best-in-class spending account with a modern user experience, real-time payment notifications, and low fees

Money management features such as spend trends, transaction categorization, and monthly spend summaries

Social features to pay your friends (e.g., Venmo) or split the bill (e.g., Splitwise)

Virtual account creation and controls (e.g., pay bills from a specific virtual account)

Access to capital through overdrafts and Monzo credit products

Access to savings accounts through marketplace partners

Premium accounts with additional software tooling and perks

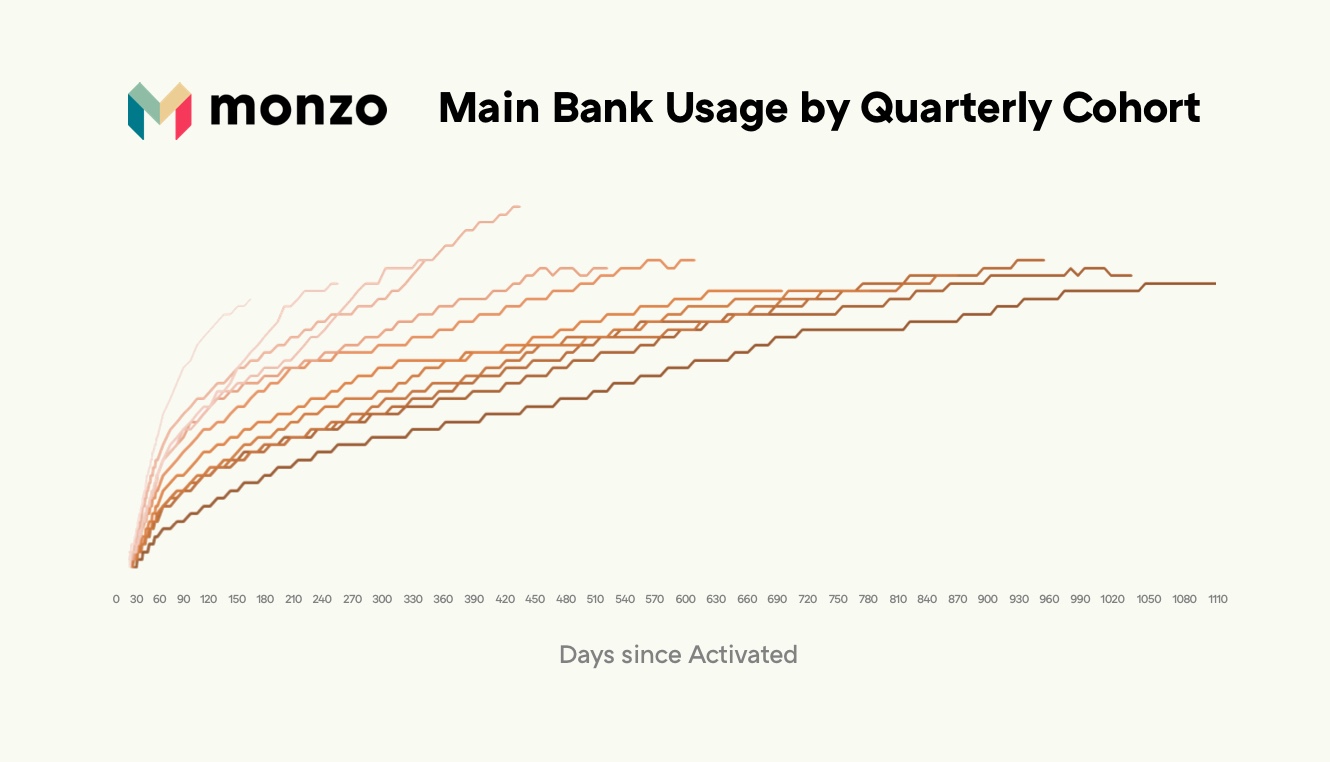

In just five years, Monzo has reached impressive density and scale in the UK with minimal marketing spend. Monzo now has over five million customers, 55% of whom are active weekly. Of those that are active, over 40% are using Monzo as their main account with this number steadily increasing in each customer cohort. TS Anil (CEO) and Sujata Bhatia (COO) joined Monzo in 2020 to further improve operational excellence in risk management, lending, regulatory and compliance. When they joined, Monzo was generating $69M in revenues (in April 2020). In the 18 months since the pandemic began, revenues have scaled to more than $200M and deposits have grown to $4B+.

In this post, we will walk through what drove Monzo’s early success, how it has come to dominate the UK market, and the company’s opportunity to change the landscape of global financial services with its beloved brand.

Early success: Foundations built on product and community

Outperforming incumbents with modern experience and digital infrastructure Monzo believed that it could solve a major concern that incumbents couldn’t: Traditional banking infrastructure does not support the convenience and modern experience that customers have come to expect in the digital age.

Monzo attacked incumbent models by creating an entirely app-based experience where customers could open a checking account from their phone for free. Monzo had the insight that customers should be able to do everything from the app. This includes storing money, sending and receiving payments, paying friends, budgeting their finances, and accessing capital via overdrafts and buy-now-pay-later (BNPL). With a Monzo account, customers do not need peer-to-peer payments apps like Cash App or Venmo, spend management tools like Mint, or BNPL services like Affirm or Klarna. Monzo provides all these services in a single easy-to-use interface. Eventually, this will extend into wealth generation tools to help customers grow their finances. Monzo’s vision is to become an all-in-one app where customers can do everything they need to from a single place.