1:28 - Tomer describes Gusto Embedded and the complexities behind compliance.</p><ul><li>Gusto Embedded takes ten years of Gusto’s experience building payroll software and compliance and makes it available to any software company wanting to ship their own payroll product to the market. </li></ul><p><strong>5:00 </strong>- Why did you decide to pursue startups as the company’s first target audience? How did you think about customer segments in that first year? </p><p><em>Over the last ten years, Gusto has scaled to build for multiple customer segments – starting with startups, then SMBs, accountants, and now with Gusto Embedded Payroll, developers who are embedding payroll directly into their software. </em></p><ul><li>When you have a grand vision, where do you start as a founder? Choose a customer segment. Make sure you choose a segment where 1) they have an important customer problem, 2) the product you are building solves that problem, and 3) you can reach your customer. </li></ul><p><strong>9:30 </strong>- Who were your competitors in the early days? </p><ul><li>The old, traditional payroll solutions, which were complex. With Gusto, <em>anyone</em> can run payroll at <em>any time</em>. Gusto also focuses on employees, a critical part of the system, by building a great payroll experience for them. </li></ul><p><strong>11:30 </strong>- Why did you decide to build for SMBs after startups? </p><ul><li>Look at your current customer base and learn from customers adjacent to the market you want to expand into. When you do expand into another vertical, make sure you maintain that early customer love. </li></ul><p><strong>14:45</strong> - How did you maintain the customer love of the existing customer segment? </p><ul><li>Think about your long-term vision and don’t put yourself in a corner when you want to move to the next segment. </li></ul><p><strong>17:00</strong> - Most startups find it hard to tackle the SMB market. Why do you think this is the case? </p><ul><li>Traditionally SMBs are hard to reach and use incomplete or manual solutions. Since 2000 an entire generation of business owners had to learn to trust online financial services. Today, SMBs are online and looking for solutions.</li></ul><p><strong>22:25 </strong>- What is different about serving SMBs as a customer versus startups? </p><ul><li>Startups come and go, and the real economics come from the big winners. Focusing on startups is a good place to start your journey, but think about how to scale with them.</li><li>There are more small businesses than startups, and they are around for a long time – but most don’t grow to thousands of employees. You need to build a business model that works with that dynamic. </li></ul><p><strong>27:00 - </strong>Why did you pursue developers and how did you decide to service them? </p><ul><li>For many verticals, it is much better to have an all-in-one platform to run your small businesses. But payroll is really hard to build yourself. Gusto Embedded helps partners deliver a more integrated solution for customers without investing the several years and tens of millions of dollars.</li></ul><p><strong>29:00 </strong>- Gusto went from directly acquiring small businesses as customers to creating an embedded solution – essentially “giving up” the relationship with the customer. How did you think about that? </p><ul><li>Evaluate the future of the industry and don’t ignore reality. Be the one to create that future. In this case, many payroll customers want all-in-one solutions. We can either try to meet those needs directly, or empower hundreds of partners to customize unique solutions.</li></ul><p><strong>33:00 - </strong>How should founders think about who to partner with? When should founders build directly for the industry and when should they go the embedded route? </p><ul><li>Think about the unique insight you have in the business you’re creating and make sure you own your destiny around that insight.</li><li>For your customer, what does a successful product look like, and could you partner with a company to fulfill those needs.</li><li>Your product must be high-quality. You have to put enough resources behind whatever you own. For everything else, you must ensure you bring in the right partner. It’s all about the end-to-end experience. </li></ul><p><strong>39:30</strong> - Gusto now makes it easier for software providers to bake compliance into embedded payroll. Tomer, I think developers looking at a payroll API would assume that compliance is baked in. But there are often steps companies have to take beyond just calling APIs. Tell us if that assumption holds.</p><ul><li>Regulation can change every quarter and every year. This is built into the product. We protect the customer and make it easy for developers to ship something quickly that is compliant for the long term.</li><li>One third of the companies in the U.S. get fined for mistakes on payroll. </li></ul><p><strong>43:00 - </strong>Compliance is the hardest part of payroll to build and ultimately has to be right. It took ten years of experience in compliance to launch this into Gusto Embedded Payroll. What advice do you have for founders who are building complicated, yet essential, components for an industry?</p><ul><li>Determine the parts of your product that are highly regulated and which areas are not. Build a culture that ensures quality-first in those highly-regulated areas, as well as a culture where people can iterate quickly in other areas. You can’t build a monolithic culture.</li><li>Embrace cross functional work. </li></ul><p><strong>46:00 </strong>- In the early days of Gusto, what guidance did you provide to your engineers about building payroll? What areas could break and which areas could not break? </p><p><strong>48:40</strong> - Looking back, would you have done anything different? </p><ul><li>Start charging what you feel is the value you provide; fix downwards versus upwards. If you’re truly adding value, customers won’t hesitate moving forward at that price.</li><li>Have the humility to learn from the customer and how the market changes around you. </li></ul><p><strong>51:45 </strong>- How should founders be thinking about embedded finance and how does this market evolve over the next 5-10 years? </p><ul><li>When you build a new software system for your customer, the more connected the system is for your customer, the better it is. Embedded products enable you to do that quickly and in high quality.</li><li>Bring more solutions into your product that are driven by what your customer needs. Understand your customer’s day-to-day, and figure out how to build something that solves their entire flow instead of one segment.</li><li>If you are not making money on your product, you don’t know if there's a product market fit. If you can charge and retain a customer, then there is product market fit. </li></ul><p><strong>56:30</strong> - Outside of payroll, what are you seeing product wise offered by APIs? </p><ul><li>This space is brand new and there’s a ton of opportunity to create a product that helps customers go through the end-to-end journey successfully and solves multiple pain points – instead of the customer needing ten years of background to create a high-quality solution.</li></ul>","comment_id":"62fa7b87ab52db0001d3b656","feature_image":"/blog/content/images/2022/08/BlogTwitter-Image-Template--5-.jpg","featured":true,"visibility":"public","email_recipient_filter":"none","created_at":"2022-08-15T09:59:51.000-07:00","updated_at":"2022-08-15T11:48:12.000-07:00","published_at":"2022-08-15T11:32:19.000-07:00","custom_excerpt":"Today, more than 200,000 businesses use Gusto for payroll, employee benefits, talent management, and more. And with the recent addition of Gusto Embedded, developers now use Gusto’s APIs and pre-build UI flows to embed payroll, tax filing, and payments infrastructure into products. ","codeinjection_head":null,"codeinjection_foot":null,"custom_template":null,"canonical_url":null,"authors":[{"id":"61fe29e3c7139e0001a7106f","name":"Y Combinator","slug":"yc","profile_image":"/blog/content/images/2022/02/yc.png","cover_image":null,"bio":null,"website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/yc/"}],"tags":[{"id":"61fe29efc7139e0001a71179","name":"YC Events","slug":"yc-events","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/yc-events/"},{"id":"61fe29efc7139e0001a71170","name":"Startups","slug":"startups","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/startups/"},{"id":"61fe29efc7139e0001a71175","name":"Interview","slug":"interview","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/interview/"},{"id":"61fe29efc7139e0001a71181","name":"YC Continuity","slug":"yc-continuity","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/yc-continuity/"},{"id":"61fe29efc7139e0001a71152","name":"Founder Stories","slug":"founder-stories","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/founder-stories/"},{"id":"61fe29efc7139e0001a71176","name":"Podcast","slug":"podcast","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/podcast/"},{"id":"61fe29efc7139e0001a711b7","name":"#24","slug":"hash-24","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"61fe29efc7139e0001a71155","name":"Growth","slug":"growth","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/growth/"},{"id":"61fe29efc7139e0001a71158","name":"Leadership","slug":"leadership","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/leadership/"}],"primary_author":{"id":"61fe29e3c7139e0001a7106f","name":"Y Combinator","slug":"yc","profile_image":"https://ghost.prod.ycinside.com/content/images/2022/02/yc.png","cover_image":null,"bio":null,"website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/yc/"},"primary_tag":{"id":"61fe29efc7139e0001a71179","name":"YC Events","slug":"yc-events","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/yc-events/"},"url":"https://ghost.prod.ycinside.com/yc-founder-firesides-gusto-on-building-for-new-verticals/","excerpt":"Today, more than 200,000 businesses use Gusto for payroll, employee benefits, talent management, and more. And with the recent addition of Gusto Embedded, developers now use Gusto’s APIs and pre-build UI flows to embed payroll, tax filing, and payments infrastructure into products.","reading_time":5,"access":true,"og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"email_subject":null,"frontmatter":null,"feature_image_alt":null,"feature_image_caption":null},{"id":"61fe29f1c7139e0001a71ba2","uuid":"a2de7e9b-655c-4b88-af38-1d4df1e6630f","title":"Meet 8 YC startups that are hiring right now","slug":"meet-8-yc-startups-that-are-hiring-right-now","html":"<!--kg-card-begin: html--><p>Many YC startups are actively hiring on <a href=https://www.ycombinator.com/"https://www.workatastartup.com/">Work at a Startup</a> across engineering, product, design, marketing and more. We asked founders to shoot a 30-second video describing their businesses and open roles. Meet them below:</p>\n<p><iframe loading=\"lazy\" width=\"560\" height=\"315\" src=https://www.ycombinator.com/"https://www.youtube.com/embed/videoseries?list=PLQ-uHSnFig5P_7Vrgb-hrPRnA6tqyX233\%22 frameborder=\"0\" allow=\"accelerometer; autoplay; encrypted-media; gyroscope; picture-in-picture\" allowfullscreen></iframe></p>\n<p>About each company:</p>\n<ul>\n<li><a href=https://www.ycombinator.com/"https://www.workatastartup.com/directory/1884/">Curebase is a CRO and software platform for distributed clinical trials. <em>Hiring: Software Engineer, Trial Manager and Product Manager.</em> </li>\n<li><a href=https://www.ycombinator.com/"https://www.workatastartup.com/directory/1276/">Curtsy makes it easy for women to buy and sell clothes from their phone. <em>Hiring: Product Design and Software Engineer.</em> </li>\n<li><a href=https://www.ycombinator.com/"https://www.workatastartup.com/directory/76/">OneSignal creates developer APIs for push notifications, in-app messaging, and email. <em>Hiring: Front-end, Mobile, Back-end and Senior Engineers.</em></li>\n<li><a href=https://www.ycombinator.com/"https://www.workatastartup.com/directory/13332/">PostEra provides chemistry-as-a-service to design and synthesize molecules faster and at a lower cost. <em>Hiring: Software and ML Engineer.</em></li>\n<li><a href=https://www.ycombinator.com/"https://www.workatastartup.com/directory/12660/">Rosebud AI</strong></a> creates software generated photos for advertising and marketing. <em>Hiring: Deep-learning Engineer.</em></li>\n<li><a href=https://www.ycombinator.com/"https://www.workatastartup.com/directory/12609/">Soteris creates ML software to route and price insurance risk. <em>Hiring: ML and Back-end Engineer.</em> </li>\n<li><a href=https://www.ycombinator.com/"https://www.workatastartup.com/directory/989/">Tovala makes home-cooked meals effortless. <em>Hiring: Software Engineer, Marketing, and Social Media Manager.</em> </li>\n<li><a href=https://www.ycombinator.com/"https://www.workatastartup.com/directory/13146/">Eternal is a rewards program for gamers. <em>Hiring: Product Design and Front-end Engineer.</em> </li>\n</ul>\n<p>And if you’re looking for a new job, apply with a single profile to over 400 YC startups on <a href=https://www.ycombinator.com/"https://www.workatastartup.com/">Work at a Startup</a>.</p>\n<!--kg-card-end: html-->","comment_id":"1104267","feature_image":"https://images.unsplash.com/photo-1542744173-8e7e53415bb0?crop=entropy&cs=tinysrgb&fit=max&fm=jpg&ixid=MnwxMTc3M3wwfDF8c2VhcmNofDU3fHxoaXJpbmclMjBub3d8ZW58MHx8fHwxNjQzOTM0NzEz&ixlib=rb-1.2.1&q=80&w=2000","featured":false,"visibility":"public","email_recipient_filter":"none","created_at":"2020-04-09T04:59:26.000-07:00","updated_at":"2022-06-27T13:08:02.000-07:00","published_at":"2020-04-09T04:59:26.000-07:00","custom_excerpt":null,"codeinjection_head":null,"codeinjection_foot":null,"custom_template":null,"canonical_url":null,"authors":[{"id":"61fe29e3c7139e0001a710bf","name":"Ryan Choi","slug":"rchoi","profile_image":"//www.gravatar.com/avatar/36ba914c5f191f813e96db0296154469?s=250&d=mm&r=x","cover_image":null,"bio":"Ryan works with YC companies to find great engineers — from 2-person startups to larger ones like Airbnb, Stripe and Instacart.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/rchoi/"}],"tags":[{"id":"61fe29efc7139e0001a71170","name":"Startups","slug":"startups","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/startups/"},{"id":"61fe29efc7139e0001a71172","name":"Video","slug":"video","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/video/"},{"id":"61fe29efc7139e0001a71171","name":"Work at a Startup","slug":"work-at-a-startup","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/work-at-a-startup/"},{"id":"61fe29efc7139e0001a71178","name":"#jobs","slug":"hash-jobs","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"61fe29efc7139e0001a71177","name":"Jobs","slug":"jobs","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/jobs/"},{"id":"62b9d2f7063d2d0001f0fc2d","name":"#1884","slug":"hash-1884","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"62ba0d42063d2d0001f0fc79","name":"#1276","slug":"hash-1276","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"62ba0d42063d2d0001f0fc7a","name":"#76","slug":"hash-76","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"62ba0de1063d2d0001f0fc80","name":"#13332","slug":"hash-13332","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"62ba0de1063d2d0001f0fc81","name":"#12660","slug":"hash-12660","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"62ba0de1063d2d0001f0fc82","name":"#12609","slug":"hash-12609","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"62ba0de1063d2d0001f0fc83","name":"#989","slug":"hash-989","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"},{"id":"62ba0de1063d2d0001f0fc84","name":"#13146","slug":"hash-13146","description":null,"feature_image":null,"visibility":"internal","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/404/"}],"primary_author":{"id":"61fe29e3c7139e0001a710bf","name":"Ryan Choi","slug":"rchoi","profile_image":"//www.gravatar.com/avatar/36ba914c5f191f813e96db0296154469?s=250&d=mm&r=x","cover_image":null,"bio":"Ryan works with YC companies to find great engineers — from 2-person startups to larger ones like Airbnb, Stripe and Instacart.","website":null,"location":null,"facebook":null,"twitter":null,"meta_title":null,"meta_description":null,"url":"https://ghost.prod.ycinside.com/author/rchoi/"},"primary_tag":{"id":"61fe29efc7139e0001a71170","name":"Startups","slug":"startups","description":null,"feature_image":null,"visibility":"public","og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"codeinjection_head":null,"codeinjection_foot":null,"canonical_url":null,"accent_color":null,"url":"https://ghost.prod.ycinside.com/tag/startups/"},"url":"https://ghost.prod.ycinside.com/meet-8-yc-startups-that-are-hiring-right-now/","excerpt":"Many YC startups are actively hiring on Work at a Startup across engineering, product, design, marketingand more. We asked founders to shoot a 30-second video describing theirbusinesses and open roles. Meet them below:About each company: * Curebase is a CRO and software platform for distributed clinical trials.Hiring: Software Engineer, Trial Manager and Product Manager. * Curtsy [https://www.","reading_time":1,"access":true,"og_image":null,"og_title":null,"og_description":null,"twitter_image":null,"twitter_title":null,"twitter_description":null,"meta_title":null,"meta_description":null,"email_subject":null,"frontmatter":null,"feature_image_alt":null,"feature_image_caption":"Photo by <a href=https://www.ycombinator.com/"https://unsplash.com/@campaign_creators?utm_source=ghost&utm_medium=referral&utm_campaign=api-credit\%22>Campaign Creators</a> / <a href=https://www.ycombinator.com/"https://unsplash.com/?utm_source=ghost&utm_medium=referral&utm_campaign=api-credit\%22>Unsplash%22},{%22id%22:%226356a9c957e9f90001984b62%22,%22uuid%22:%2232e1602f-ec89-49b0-932c-61ef6bbacfcb%22,%22title%22:%22YC Founder Firesides: Mutiny on AI and the next era of company growth","slug":"yc-founder-firesides-mutiny-on-ai-and-the-next-era-of-company-growth","html":"<p><a href=https://www.ycombinator.com/"https://www.mutinyhq.com//">Mutiny (<a href=https://www.ycombinator.com/"https://www.ycombinator.com/companies/mutiny/">YC S18</a>) uses AI and data to convert website visitors into customers. Today, the fastest growing B2B companies such as Notion and Snowflake use Mutiny to identify ideal customers, determine sections of websites that will increase conversion, and produce copy that converts visitors into customers. </p><p>YC’s <a href=https://www.ycombinator.com/"https://twitter.com/anuhariharan/status/1557784730543632384/">Anu Hariharan</a> sat down with Mutiny co-founder and CEO <a href=https://www.ycombinator.com/"https://twitter.com/jalehr/">Jaleh Rezaei</a> to talk about their <a href=https://www.ycombinator.com/"https://twitter.com/jalehr/status/1582352047659024385/">recent acquisition</a> of Intellipse, an AI marketing platform, as well as how AI will impact the next era of growth. Throughout, Jaleh shares advice about acquisitions as a growth strategy and evolving your product with AI. </p><p>You can listen here or on <a href=https://www.ycombinator.com/"https://open.spotify.com/episode/7dy1qB7XQfOryE4kj4spGS/">Spotify, <a href=https://www.ycombinator.com/"https://podcasts.apple.com/us/podcast/160-yc-founder-firesides-mutiny-on-ai-and-the-next/id1236907421?i=1000583708925\%22>Apple Podcasts</a>, and <a href=https://www.ycombinator.com/"https://twitter.com/i/spaces/1yNxaNzAPPnKj/">Twitter.

Brex: The Future of Business Finance and Cash Management

by Anu Hariharan, Nic Dardenne4/26/2021

When Henrique Dubugras and Pedro Franceschi joined the YC W17 batch with an idea for a VR startup, they quickly encountered a problem. They had applied for a business credit card to help fund software and other expenses and were denied. Business credit is traditionally underwritten based on the founders’ FICO scores. As international founders with less than a month of credit history, their chances of getting approved were slim to none, despite having $125K in the bank.

It wasn’t just them. They discovered that, while early startup founders had access to high-fidelity payments products like Stripe (YC S09) right from the get-go, getting access to basic cash management and credit products was a terrible experience for everyone. Even with $125K from YC and $1–2M in venture funding, a startup’s credit limit is still likely to tap out at $20K from an incumbent creditor—which is not nearly enough to cover software, marketing, and other expenses. Cards are particularly a must have for young companies because large vendors don’t often accept ACH and other forms of alternative payment from early startups. In practice, this leads to founders resorting to using their personal credit cards for SaaS subscriptions or digital marketing, and filing reimbursements regularly.

Stripe also set a great example in how they transformed the internet’s payment infrastructure. Stripe’s launch in 2009 made it possible for startups to easily collect payments online via developer-friendly APIs. Over time, Stripe has expanded to support more business models (e.g., ecommerce, SaaS, marketplaces) and verticals.

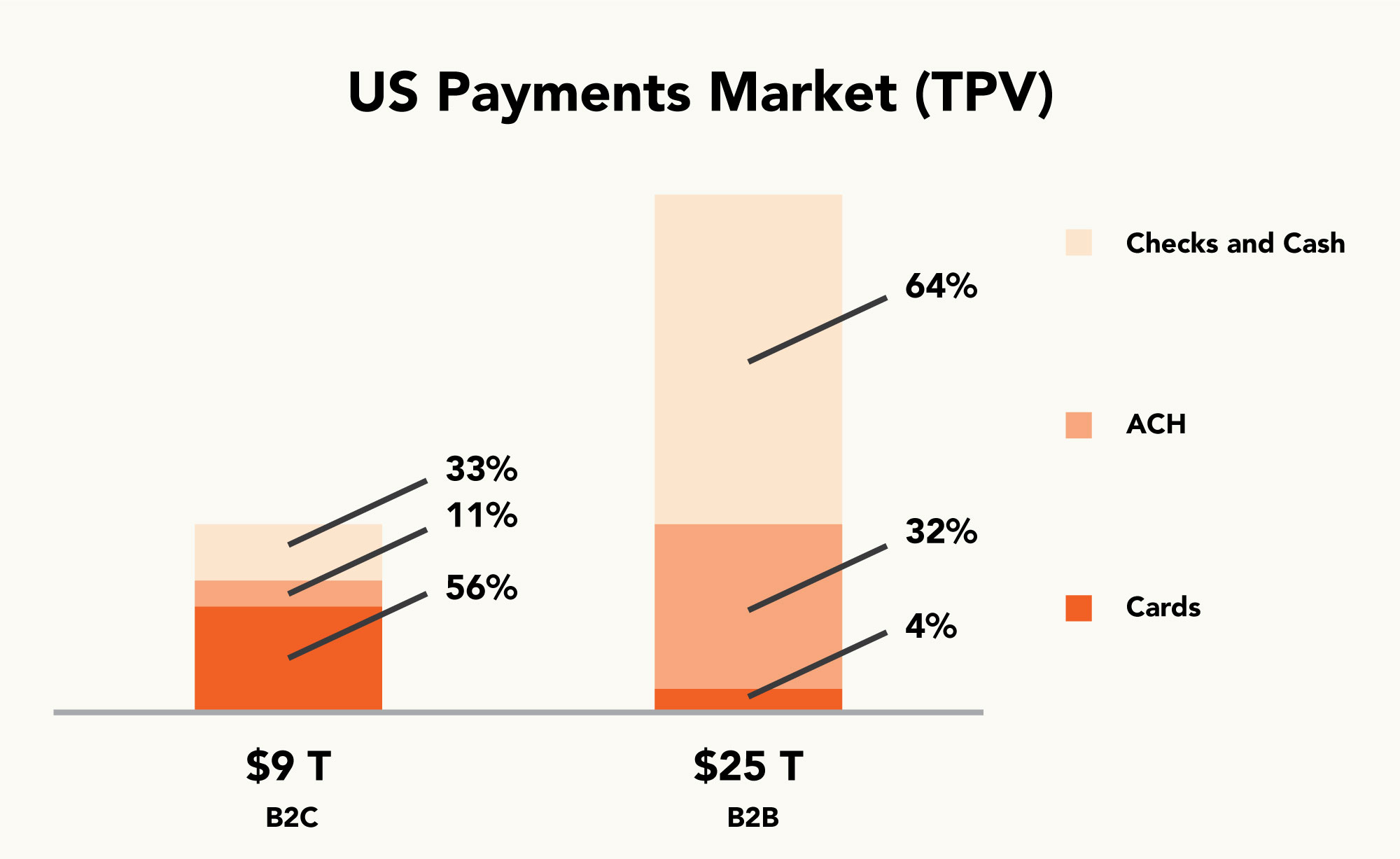

While products like Stripe and Square have dramatically pushed business-to-consumer (B2C) transactions to credit cards, business-to-business (B2B) card penetration has remained stubbornly low. The US B2B payments market is three times the size of the B2C market—yet B2B digital payments penetration is 36%, half as much as B2C (67%). B2B credit card adoption is especially low, accounting for only 4% of the market.1

The extremely low penetration of credit cards in the B2B space is a historical remnant of the industry. Checks remain the most popular payments channel because, in addition to being simple and virtually free to use, they’ve been around the longest. ACH came next in the 1970s and now makes up half the payments volume as checks (mostly in recurring payments such as payroll and billing).

Meanwhile, card adoption is only 4% not for a lack of demand, but because of the significant friction in the accessibility, onboarding, and utility of the product. Most banks and card providers ask for excessive documentation, take 3–5 days to onboard customers, and require a personal guarantee from business founders and owner-operators. Even then, the credit limits they offer are minimal, since they’re being underwritten on the personal credit history of the founder and not the health of the business. And a further obstacle: the walled garden of most enterprise resource planning (ERP) systems makes it difficult for new payment solutions to readily integrate with a company’s accounting software, adding administrative cost to reconciliations and making the total cost of introducing a new payment system incredibly high for small businesses.

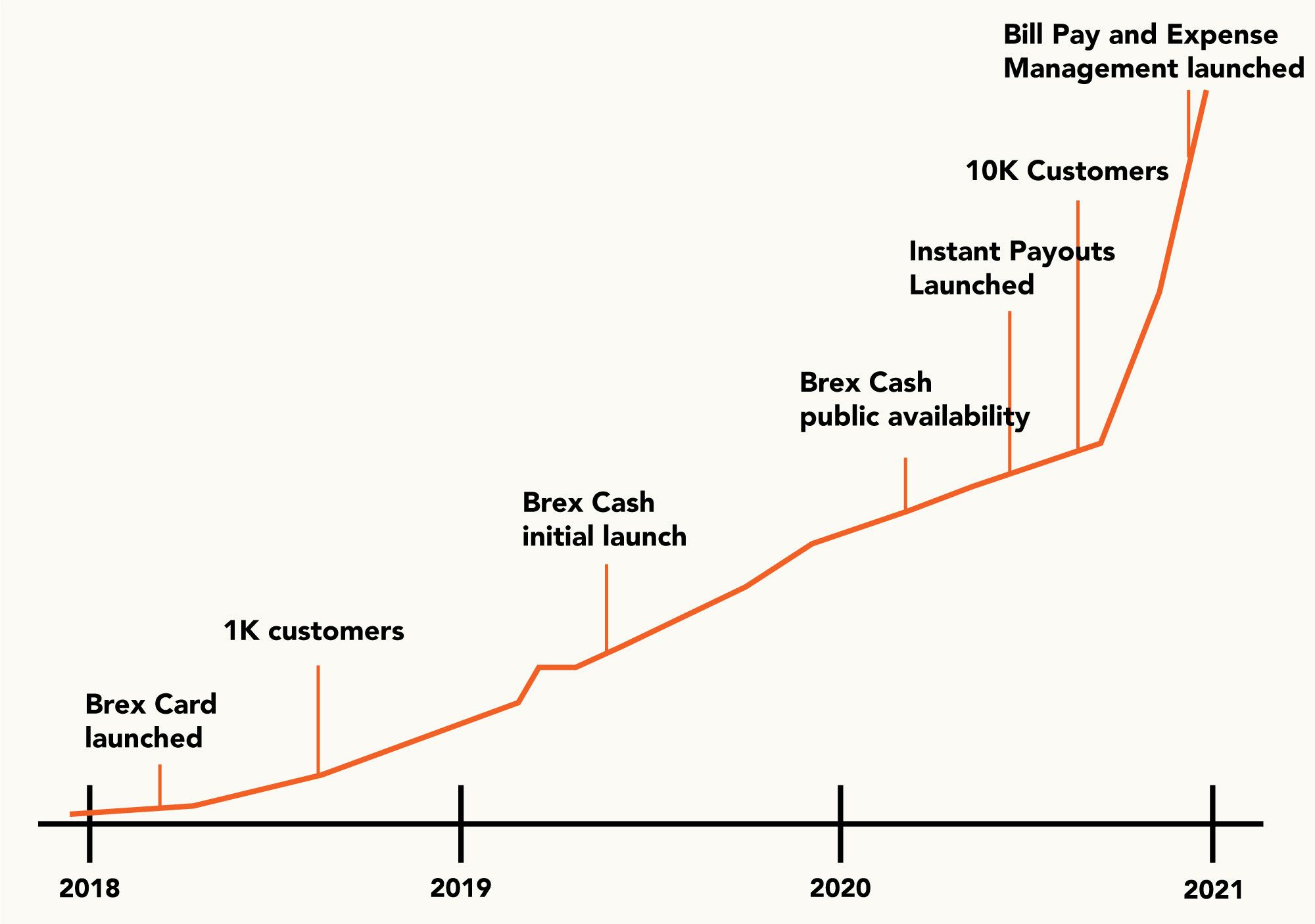

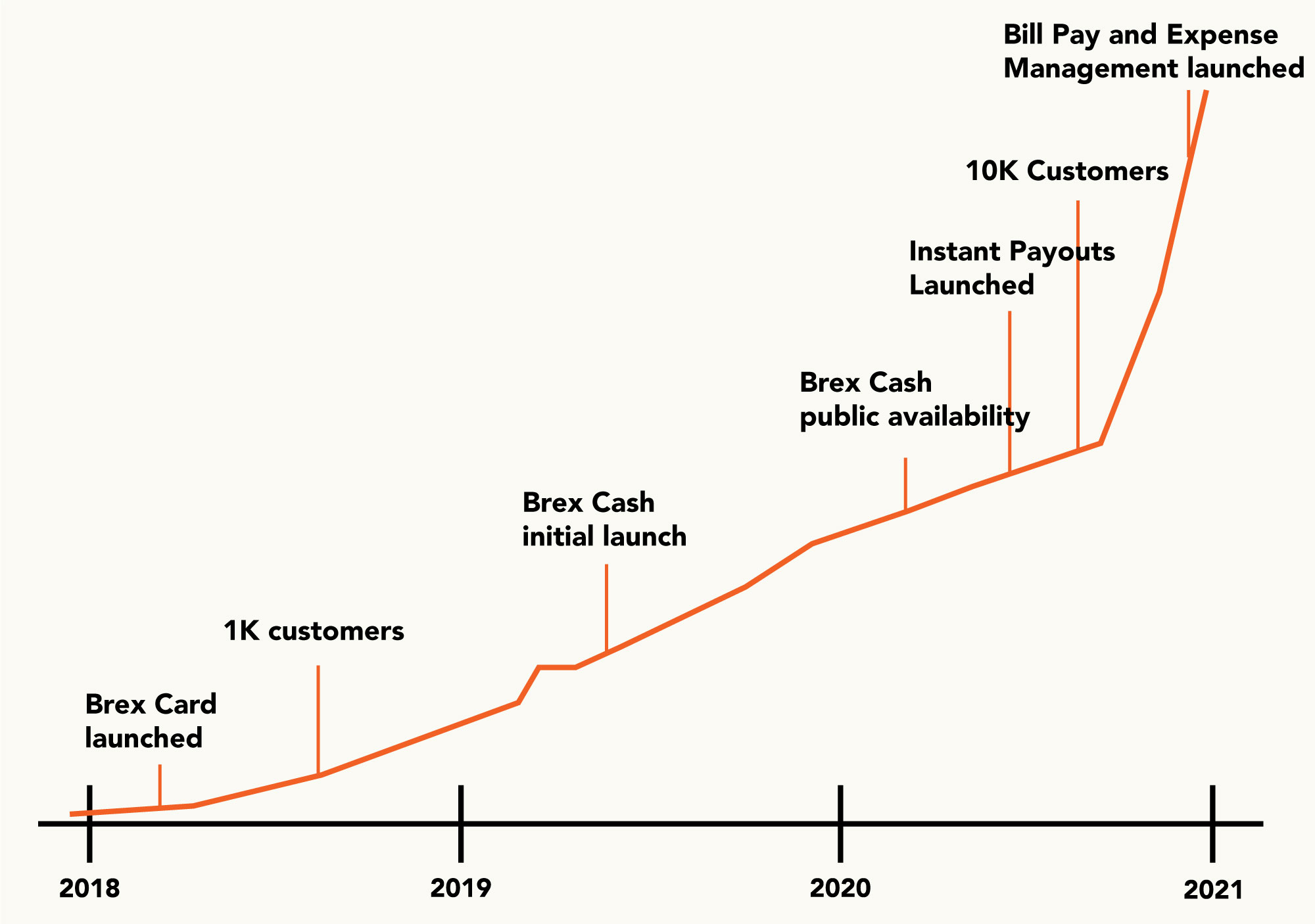

To address this massive underappreciated market opportunity (not to mention a personal pain point), Henrique and Pedro pivoted and built Brex. They had the benefit of having previously founded a Stripe-like payments company as teenagers in Brazil. They had scaled that company to $1B+ in annual payments volume, then sold it. Having already developed an understanding of the initial card infrastructure stack needed to build Brex, they were able to move fast and launched their first product within six months.

The initial Brex product was a simple 30-day charge card for startups with credit limits based on cash balance. The value proposition was clear: Founders didn’t have to personally guarantee, it took less than 24 hours to get approved, and businesses could access 10–20x higher credit limits since underwriting was based on cash balance. They further differentiated the product with several intuitive features. Brex gave startup founders a daily view into the month’s cumulative expenses (vs. incumbent offerings which only offered end-of-month reconciliation). They made it 10x easier to file expenses: whenever an employee used their Brex Card to pay for something, they instantly got a text that let them immediately send in the receipt (vs. having to deal with saving receipts and filing them all at the end of the month). Lastly, they designed a rewards program for startups, offering customers things like rewards on SaaS spend and discounts on AWS and Zoom.

Brex’s product-market fit was instantaneous, and the product has spread like wildfire among venture-backed startups. Within five months of launching, Brex grew from 100 to 1,000 customers. In the less than three years since launching, they’ve scaled to over 20,000 customers (including 60% of all YC companies).

Henrique and Pedro’s vision for Brex isn’t just to issue credit cards to startups—it’s to become the financial operating system for growing businesses. We believe that Brex’s experience represents the next great shift in global B2B financial transactions.

The Beginning: Removing friction to unlock demand

Early on, Brex understood that removing the friction of financial products could meaningfully differentiate them from the status quo. Brex’s initial insight was simple: “You should be able to sign up for a credit card and other financial services as easily as you can set up an email address—in minutes, all online.” Once they began to onboard customers, Brex found that the demand for seamless finance was even bigger than they had initially imagined.

To provide the modern and seamless service they envisioned, Brex built a risk assessment system that was fundamentally different from traditional credit card underwriting. They removed the paper-based back-and-forth of traditional KYC2 processes and built systems that could collect and verify critical business information (like beneficial ownership) in seconds. They then built their own ledger that used real-time cash, operating, and transaction data to underwrite customers to credit limits with multiple levels of authorization. Incumbent underwriters rely on point-in-time data and must build confidence in customers over long periods of time. Brex’s digital approach enabled them to instantly onboard customers with 10-20x higher credit limits than incumbents were able to offer. These methods have proven to be highly efficient: Brex’s credit losses have been lower than those of Amex and Silicon Valley Bank, even when including the impact of COVID-19.

Demand for frictionless financial services soon spread far beyond venture-backed startups. Every month, more than 10,000 businesses across the country were signing up. But because their underwriting system was built for tech startups, Brex had been turning away more than 80% of those potential customers. In late 2020, Brex decided to retool their system to serve more customer segments.

With the average business in mind, Brex launched a new risk system that could instantly onboard any legitimate business to a cash management account and a same-day charge card (a debit card-like product). This change enabled Brex to grow new monthly customers tenfold, and they were able to maintain instant same-day approvals for 80% of those customers. In the first quarter of 2021, Brex onboarded more customers than it did in the entire history of the company and. Today, more than 70% of new customers are traditional small and medium businesses.

Today: Scaling from cards to cash management and financial software tools

The next act for Brex was to launch complementary financial and software products beyond credit cards. Last year, they launched a service that transformed the trajectory of their platform: Brex Cash. Brex Cash was imagined as a bank account replacement product that would let Brex serve companies even before they qualify for credit. It was also a way for customers to send checks, ACH, and wire payments to vendors and third parties that didn’t accept credit cards (remember, 96% of B2B payments in the US are non-card).3

But Brex Cash is not just an add-on product. It is a deeply integrated solution that reimagines and streamlines workflows for various forms of payments.

Brex designed Brex Cash to be the center of a company’s financial operations, rather than an account used solely for financial services. This meant that the product had to be intuitive and designed for daily use. Brex removed all fees on ACH and wires, improved payment speed and user flows (Brex’s payment initiation is 40–50x faster than competitors’), and built in utility beyond financial services. For example, they’ve drastically reduced customers’ accounting workloads by integrating Cash into third-party accounting systems. These integrations have made it possible for SMBs like OP2 to save the 20–30 hours a week they previously spent downloading bank statements and doing manual reconciliation.

Today, Brex has more than 10,000 customers ranging from small venture-backed startups and traditional SMBs to large growth-stage businesses using both Brex Cash and the Brex Card. In our view, Cash is the foundational product that is transitioning Brex from a card-issuing company to an all-in-one finance operations platform.

As Brex has scaled, so have their customers. Many of their early startup customers have grown into large organizations whose needs have evolved past simple credit cards. To keep up with customers, Brex has moved quickly to shift from a team-centric product to an enterprise product. They’ve created department- and category-level tracking tools where leadership and finance teams can better understand organizational spend against budgets. Companies can now also use Brex’s virtual cards infrastructure to issue cards to specific organizations and employees rather than dealing with individual reimbursements. This alone translates to hours of time saved for employees and finance teams. Today, large startups like Scale AI (YC S16), Rippling (YC W17), Rappi (YC W16) and Flexport (YC W14), among many others, use Brex as a central tool for managing finances.

The future: All-in-one finance

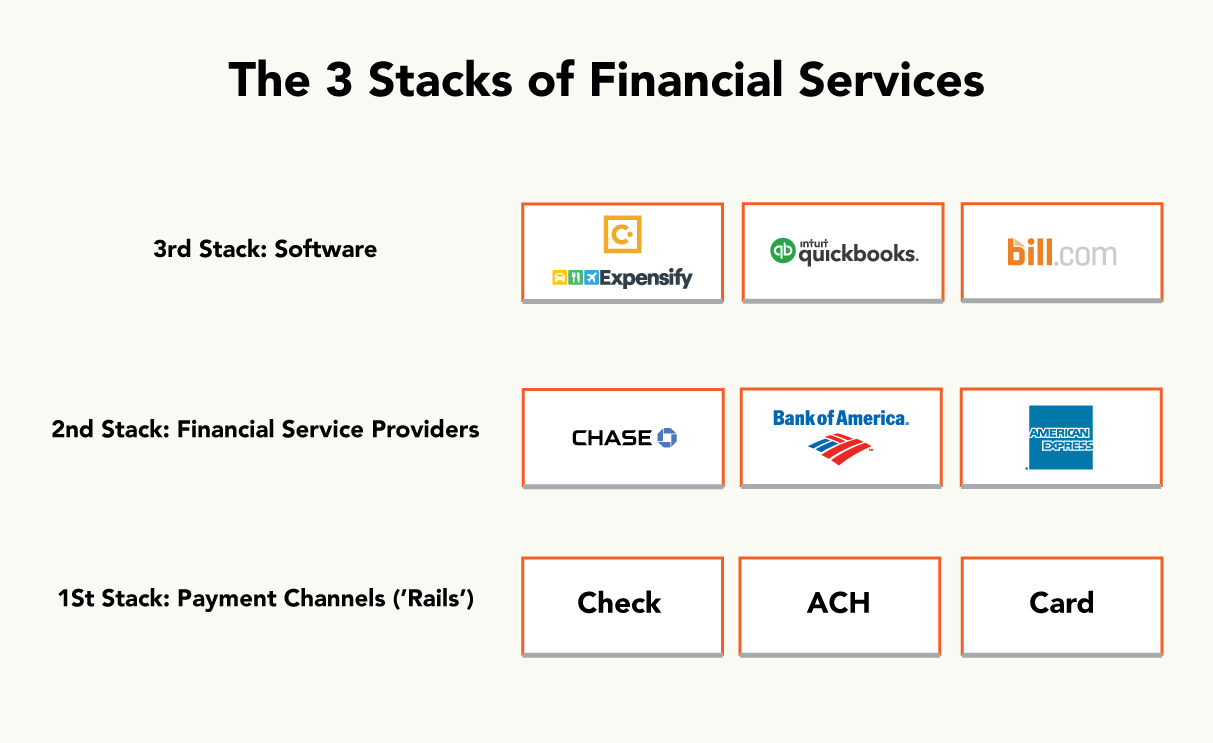

With more and more companies using Brex Cash, Brex is on its way to becoming a first of its kind all-in-one finance platform. Historically, financial operations software and financial products have existed separately. The incumbent system involves three key “stacks.” The first stack is the payments infrastructure (checks, ACH, and card networks) that processes transactions. The second is the access providers to the underlying infrastructure—institutions like Amex and Chase that manage the storage and movement of funds. Finally there is the value-added services stack, made up of products that handle administrative back-office tasks (such as Intuit, Bill.com, and Concur).

Because of how this system is designed, the average SMB uses at least six different financial services and software providers to manage its business. A typical ecommerce company may use Chase for storing capital, American Express for travel and software spend, Bill.com to manage payables, Expensify to manage employee spend, Quickbooks for accounting, Shopify or Stripe for accepting payments, and a third-party lender for a longer-term working capital financing product. While all these solutions do have the ability to talk to each other, there is no single entity that has a holistic view of the business’ financial operations.

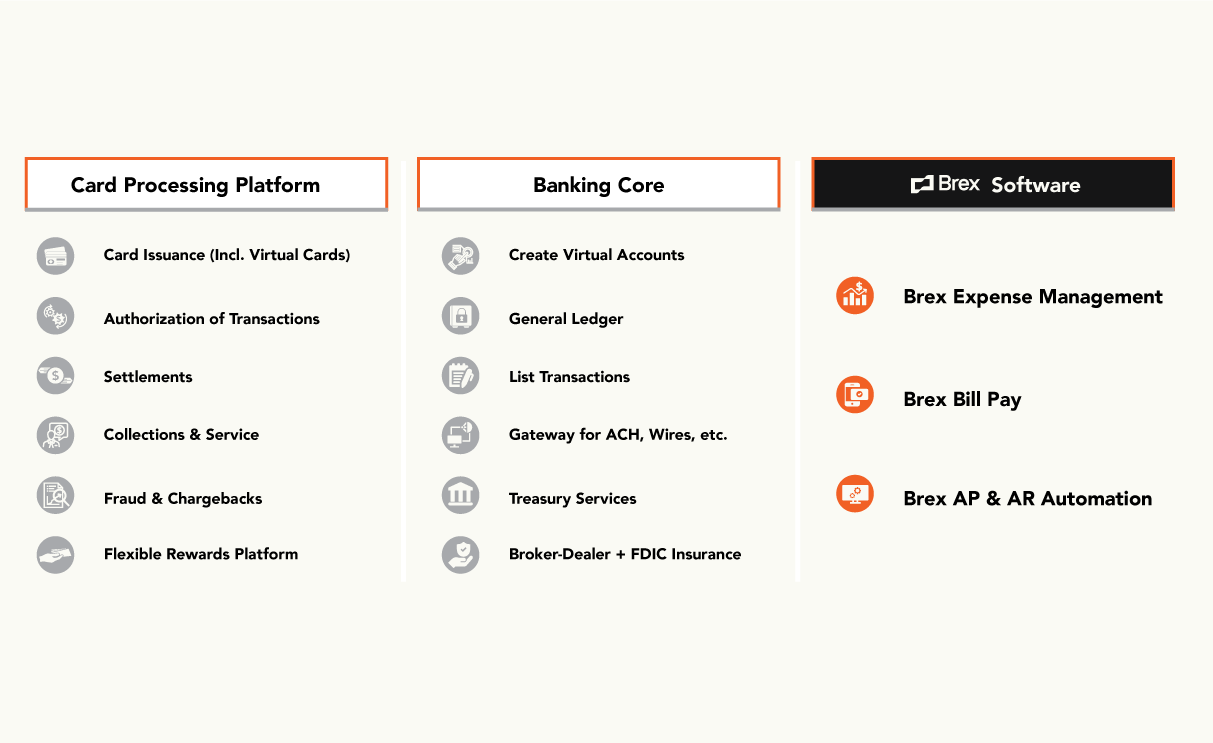

Brex is changing the landscape by combining financial products and software into a single platform. The company has spent the past two years building its card processing and cash management infrastructure, which in turn will power its software (e.g., Expense Management, Bill Pay). Enabled by its financial infrastructure, Brex is building the “financial operating system” for growing businesses, enabling them to spend and track payments across all mediums.

We are already seeing how integrating the financial stack is enabling greater access to financial resources and only expect these resources to improve as Brex moves closer to a true all-in-one finance platform.

By owning both software and financial infrastructure, Brex is able to:

(1) Leverage customer data to offer better financial products than competitors: When customers make the free Brex Cash account their primary operating account, Brex gains full visibility of their customers’ financial health. Currently, Brex uses this data to predict estimated runway and dynamically sets credit limits that can be up to 10–20x more than what legacy competitors offer. Datrics (YC W21) uses both Brex Cash and Card for this reason. In the future, Brex could identify startups and SMBs that serve “safer” customers (i.e., large enterprises) and leverage repayment data and relationship history to offer bill discounting/invoice factoring and other credit products.

(2) Drive deep value for customers via software: The payment workflow integrations that come with the Spend Management software effectively deliver a product that is not just a system-of-record but also a system-of-engagement for customers. This drives immense value not just through lower fees but cost savings and more efficient operations across the board. Back-office administrative teams spend significant hours in manual processes like standardizing invoices, matching invoices to purchase orders, managing billing information for several vendors, payment approvals, and accounts reconciliation/reporting. By integrating the financial stack, Brex can automate these processes, saving companies time and money.

(3) Build unique financial products: Building on its positioning as both a software and financial services provider, Brex can offer financial services products that are not readily available from incumbents. There is no better example of this than Instant Payouts, which launched in Q4 of 2020. An ecommerce merchant can instantly settle funds through the click of a button in their Brex dashboard, instead of waiting two weeks for the revenue to be distributed to their account. Funds are instantly disbursed in exchange for a fee that can be paid with Brex Card points. This is incredibly valuable because it enables ecommerce sellers to smooth out their cash flow and reinvest it in growth regardless of the selling platform. While the customer-facing product is simple, the backend infrastructure is sophisticated, integrating Brex Card, Cash and underwriting stacks.

(4) Lower the cost for customers: As a financial services provider and a software company, Brex is disrupting existing pricing models of point solutions in both layers. By monetizing customers through card interchange fees, Brex is able to price software far lower than a pure SaaS competitor can charge. An SMB with 20 employees may have to pay ~$4,200 per year for Expensify, Bill.com, and Quickbooks. Brex customers can pay a tenth of that in fees and get all of their spend data in a single place. Brex can choose to give even more value back to customers by making any of its products loss leaders to encourage new transactions on the platform. For example, Brex does not charge fees on any bank or wire transfers today, an unconventional practice among incumbents.

(5) Launch customer-centric products faster: By limiting reliance on third parties, Brex can build and launch products faster. In less than two years, the company has been able to quickly expand from a single-product company to a multiproduct company (Card, Cash, Instant Payouts, Bill Pay, and Expense Management) because they own everything from the general ledger to the credit box and can quickly build on their own infrastructure.

As Brex scales, its data-driven underwriting algorithm will benefit immensely from an expanding customer base that feeds back into the company’s models. Over time, this should yield a lower-delinquency credit book. On the flip side, the diversification of the credit book and seasoning across economic periods should yield cheaper cost of capital over time, which will translate to higher margins for Brex and/or lower pricing for its customers. Brex is also among the first fintech companies (and the first in a B2B use case) that has filed for an industrial loan charter, which will allow Brex Cash to transform into a full-fledged “business bank.” With the ability to lend using Brex Cash customers’ deposits, Brex will be able to provide loans and credit cards at a lower cost of capital.

The financial upsides of an integrated system are significant. The overall infrastructure and ease of use create more capital for both small and growing businesses. Digitizing B2B finances can entirely change the trajectory of a business. OP2 uses both Brex Cash and Card because the combination enables credit limits three times higher than the next competitor, which has allowed the company to meaningfully grow. We see the future of Brex as existing hand-in-hand with the future of growing businesses.

Conclusion: The inevitability of digital B2B payments

In the past decade, we’ve seen the emergence of large players that have reduced friction and enabled digitization of consumer-to-business (C2B) payments by helping both consumers pay digitally (Cash App and PayPal) and helping merchants accept digital payments (Square and Stripe). Meanwhile, B2B payments account for nearly 3x the volume of C2B and the electronic payment penetration is fractional in comparison. The digitization of B2B payments is inevitable in the decades to come.

There is no one way to address this problem, and the market has a spectrum of use cases that need to be addressed. This is also not a zero-sum game; we believe the $25T B2B payments market is large enough to support several companies. Brex is only one of the companies that has revealed the underlying demand and it has only grown more desperate in COVID. In a recent Mastercard study of payment type usage during the pandemic, online card payments saw the greatest increase (+60%) while cash (-34%) and checks (-24%) decreased the most. Legacy players’ archaic infrastructure and high-fee models have created a natural ceiling for how many businesses they can service. Just like consumer payments adoption, we believe that the majority of digital payment adoption will be led by Brex and other modern fintech companies, such as Modern Treasury (YC S18) and Routable (YC S17). We are excited about the next decade of B2B payments and believe many new multibillion-dollar businesses will emerge.

Thank you to the Brex team, Mia Mabanta, and Chloe Gordon for reading multiple drafts of this essay, and to Zain Ali for designing the graphics.

Notes

1. Mastercard, SunTrust – Electronic B2B Payments: The Next Frontier ↩

2. Know-Your-Customer, a standard customer identity verification process ↩

3. Mastercard, SunTrust – Electronic B2B Payments: The Next Frontier ↩

Companies Mentioned

Other Posts

Authors

Anu Hariharan

Anu is a Managing Director & Partner at YC Continuity. Previously, Anu was a Partner at a16z, where she worked actively with the management teams of companies including Airbnb, Instacart, and Medium.

Nic Dardenne

Nic is a principal at YC Continuity. Nic has helped support the teams at Brex, Convoy, Faire, Groww, Monzo, Rappi, Segment, Snapdocs, and Vouch. Before YC, Nic worked as an analyst at Morgan Stanley.